Take-home grocery sales in Ireland increased by 4% in the four weeks to 14 April 2024, according to our latest data. April was the strongest month with shoppers spending more in-store than usual in preparation for the Easter and school holidays. Volumes per trip increased slightly by 0.4% as did visits to store (up 1%), with shoppers making 21.5 trips on average over the month of April. Average price per pack grew more marginally this month at 0.7%.

Grocery inflation stands at 2.9% in the 12 weeks to 14 April 2024, down 12.9 percentage points compared to April 2023. Although value sales are up this month, grocery price inflation is the real driving factor behind this rather than increased purchasing.

This is the twelfth month in a row that there’s been a drop in grocery inflation, so more good news for consumers. It’s the lowest inflation level we have seen since March 2022. What’s more, our latest pressure group survey* shows that Irish consumers have a more positive outlook with fewer people struggling financially thanks to the easing of inflationary pressures. Around a quarter of shoppers admit they are still struggling, and while this is still significant, it’s a big improvement on the 32% who reported the same last October.

On the hunt for Easter Egg bargains

Shoppers in Ireland remained on the hunt for value when it came to their Easter purchases with 24.9% of sales going through the till being for items on promotion, down 3.7% since January 2024. This was higher for Easter Eggs, with over 43% of value sales on promotion.

Retailers also pushed own label lines to get Irish shoppers through the doors. Sales of own label products performed strongly, growing ahead of the total market at 6.5% year-on-year and holding value share just shy of 48%. Over the latest 12 weeks, shoppers spent an additional €97m year-on-year. Premium own label ranges also performed well with shoppers spending an additional €18.7m on these lines year-on-year, and growth of 12.9% when compared to this time last year. Brands also saw growth over the 12 weeks at 3.9%, slightly behind the total market.

An early Easter didn’t affect seasonal confectionary sales this year as spending topped €23.9 million for the first time ever in the days leading up to Easter Sunday. While rising prices played a major role, the number of chocolate Easter eggs sold in the seven days to Easter was also 22% higher than this time last year with nearly 34% of Irish consumers buying one during this period. A record €9.9 million was spent on Easter eggs alone, while many also opted for hot cross buns with shoppers spending over €1 million over the week, up 7.7% on last spring.

Online sales were up 19.5% year-on-year with shoppers spending an additional €33 million on the platform. New shoppers contributed an additional €14.1 million to online’s performance alongside more frequent and larger trips boosting online’s performance.

Irish retailer performance update

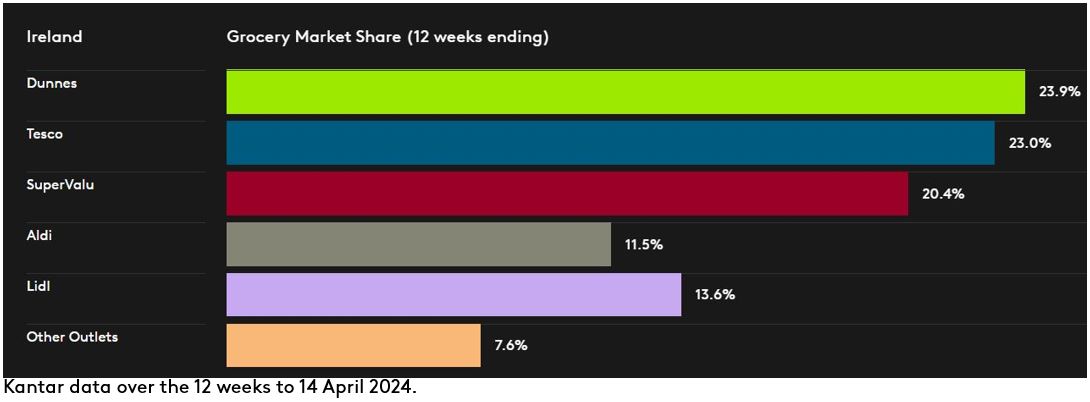

Dunnes holds 23.9% market share with growth of 8% year-on-year. Dunnes growth stems mainly from more frequent trips, up 4.1%, together with new shopper recruitment, which contributed a combined €32.8 million to their overall performance.

Tesco holds 23% of the market, up 7.6% year-on-year. Tesco has the strongest trip frequency growth amongst all retailers, up 8.9% year-on-year, which contributed an additional €62.3 million to their overall performance.

SuperValu holds 20.4% of the market with growth of 3.5%. SuperValu shoppers make the most trips in-store compared to all retailers, an average of 21.8 trips and with strongest growth in volume per trip amongst all retailers, up 5.8% which, contributed an additional €37.4 million to their overall performance.

Lidl holds 13.6% share with growth of 6.4% year on year. More frequent trips contributed an additional €33 million to its overall performance. Aldi holds 11.5% market share. New shopper recruits alongside more frequent trips contributed an additional €8.4 million to their overall performance.

Want more like this?

Read: Easter sales spring market growth

Read: Love is in the air as Irish shoppers indulge for valentines