Following a record-breaking festive period in December 2023, take-home grocery sales are starting to slow with a more moderate 2.2% increase in the four weeks to 21 January 2024, according to our latest data. In January, the average price per pack rose 3.7%. Although sales have slowed compared to last month’s mammoth 7.8% increase, shoppers still spent an additional €21.4m compared to the same time last year.

Grocery inflation stands at 5.9% in the 12 weeks to 21 January 2024, which is down 1.2 percentage point compared to 7.1% in December.

Many Irish consumers are keeping a very close eye on their purse strings after indulging over the festive period and to help manage household budgets, many are trading down to supermarket’s own label products and looking for deals. The amount of sales on promotion has grown by 9.9% year-on-year with shoppers spending €92.6 million more than last year with, meaning that 28.9% of all value sales this period were on promotion.

Sales of own label lines are performing strongly and growing ahead of the total market at 8% year-on-year, holding value share of 44.9% and with shoppers spending an additional €117m year-on-year.

Premium own label ranges also performed well with shoppers spending an additional €157m on these lines with growth of 10.3% when compared to this time last year. Brands also saw growth over the 12 weeks of 5.2%, but this is slightly behind the total market.

New year, new resolutions

Health always becomes a top priority after an indulgent festive season, with many Irish consumers kicking off 2024 with good intentions. Shoppers cut back in more ways than one this month. Across Ireland consumers took on ‘Dry January’ with alcohol sales falling by 8.6% and shoppers spending €7.4 million less during January compared to last year. Sales of non-alcoholic beverages jumped 8.9% with shoppers spending €125,000 more year-on-year. Almost 7% of Irish households purchased in the category over January with a volume increase of 3.9%.

However, Veganuary didn’t have the same impact this month. Despite nearly 38% of Irish households purchasing chilled or frozen plant-based products, sales fell 2.6% with shoppers spending €200,000 less compared to last year. With many shoppers returning to normality after the festive break, they opted for ease when adjusting to routines and, as a result, spent an additional €3.3 million on chilled convenience.

Online sales remained strong into 2024. In the 12 weeks ending 21 January 2024, sales were up 17.7% year-on-year with shoppers spending an additional €28.2 million. The main contributor was more frequent trips, which contributed an additional €12.7 million to its overall performance. Online continues to attract new shoppers with 18.5% of Irish households purchasing groceries online with volume up 0.8 per centage points year-on-year.

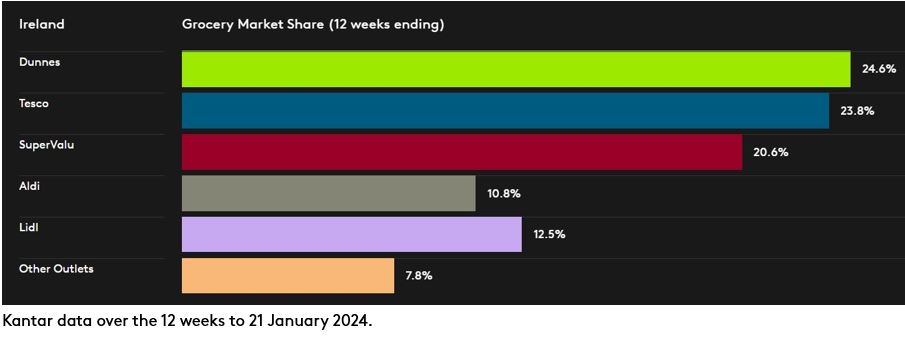

Irish retailer performance update

Dunnes, Tesco and Lidl all grew ahead of the total market in terms of value this month.

Dunnes hit a new record share of 24.6% with growth of 9.9% year-on-year. Dunnes growth stems from a boost in new shoppers, up 1.3 percentage points year-on-year which is the highest growth in new shoppers among all the retailers, and alongside more frequent trips, contributed a combined additional €38.1 million to overall performance.

Tesco holds 23.8% of the market, also a new record for the retailer, with growth of 9.4% year-on-year. Tesco had the strongest frequency of trips growth amongst all the retailers again, up 11.8% year-on-year, which combined contributed an additional €88.4 million to overall performance.

SuperValu holds 20.6% of the market with growth of 4%. SuperValu shoppers make the most trips in store when compared to all retailers, an average of 21.1 trips, contributing an additional €9.4 million to overall performance.

Lidl holds 12.5% share and growth of 8.2% year on year. More frequent trips contributed an additional €30.9 million to its overall performance. Aldi holds 10.8% share, with more frequent trips and new shopper arrivals contributing an additional €5.9 million to its overall performance.