Kantar Worldpanel’s latest figures for the 12 weeks ending 15th May 2020 reveal that consumer spending on FMCG in China recorded value growth of 1.8% compared with the same period last year, suggesting a steady recovery following the outbreak of COVID-19. In the latest four weeks, the total FMCG market achieved a robust growth of 4.6% in value. All regions showed a similar recovery trend, although the East and West regions led the rebound. Homecare categories continued their strong growth with the dairy and personal care sectors showing the strongest recovery trends.

Modern trade (including hypermarkets, supermarkets, and convenience stores) fell by 1% in the latest 12 weeks compared with last year. RT-mart maintained its leading position, posting a market share of 7.2%.

Despite a loss of shoppers over the past year, Wal-Mart started to show steady recovery as a result of opening small community stores, which are particularly focused on fresh produce and delivery services. With a reduced range of 3,000 SKUS, Wal-Mart’s community stores expanded their share of pre-packaged fresh food to 50% across all ranges. Amongst the regional players, the Bubugao group achieved an unprecedented growth rate of 8.7% in the latest 12 weeks, driven by a bigger buyer base. The retail group also fully leveraged their mini programs to attract more online traffic and build their omni-channel offer.

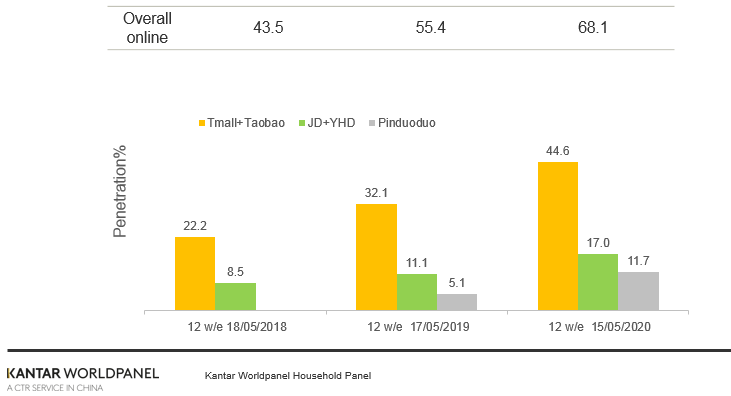

Ecommerce maintained its strong performance with a value growth rate of 42% in the last 12 weeks. The strong growth was contributed by consumers in both upper-tier and lower-tier cities.

Among the top ecommerce players, Alibaba and JD consolidated their leading position with more shoppers using their services. In the past 12 weeks, Alibaba reached a national penetration of 44.6% which is 43% higher than last year. Ecommerce players are gearing up for the 618 shopping festival and will be hoping to maximize their sales through the aggressive promotions and livestreaming events which started at the beginning of June. It is worth noting that the penetration gap between JD and Pinduoduo has been continuously narrowing. Pinduoduo’s penetration in FMCG more than doubled in the last year, with more brands setting up stores on the platform to allow consumers to make group purchases at a discounted price.