Coca-Cola remains the world’s most purchased brand for the 12th consecutive year while at-home treats define reshaped shopper behavior in 2023.

Kantar’s Worldpanel reveals the world’s most chosen brands and lays out a comprehensive view of how shopper behavior evolved around the world in 2023. With the global FMCG inflation rate halving from 8.4% in 2022 to 4% in 2023, shoppers started mixing treating and premium purchases alongside the coping strategies of 2022. Brand Footprint, Kantar’s analysis of consumer behavior in 62 markets representing 76% of the global population and 86% of global GDP, reveals that average grocery spend per household around the world exceeded $1,000 for the first time on record, almost 60% more than was spent a decade earlier in 2013.

Key insights from the 12th edition of this study include:

- Coca-Cola remains the world’s most purchased brand for the 12th consecutive year. Penetration – or the percentage of households that purchase the brand – grew 2.6%. The brand was chosen off the shelf by consumers almost 8.3 billion times.

- Red Bull was the fastest growing FMCG brand, with 17.8% growth regarding the number of times it’s purchased (1.43 billion times), thanks to more new shoppers in markets including Brazil, Mainland China, France, Germany and the US.

- Sunsilk was the world’s most successful brand in winning new shoppers, with more than 26 million new households purchasing the brand in 2023.

- Average spend on FMCG brand increased by 8.6% to $1,052 per buyer, as a result of grocery inflation that averaged 4% during the year, as well as greater at-home treats and shifts to premium purchases to offset coping strategies.

- Illustrating the inclusion of treats and premium brand products in shoppers’ repertoires, the average spend per item increased by 6.7%.

- North American shoppers spent the most on packaged FMCG products, averaging $3,063 per household, while consumers in Bangladesh spent the least, averaging less than $159.

- The mix of spending across global brands, local brands and private label groceries continues to evolve. Spending on private label goods increased by 0.5% points to reach 22.7%. Despite a fall in unit sales, global brands retained 30% of spend thanks to increased prices and premiumisation.

- ‘Shopping around’ continued as a coping strategy as shopping trips increased by 2.4%. ‘Discount Grocery Stores’ increased their share of shopper spend by 10.3% to reach 16% share globally (and 24.5% in Western Europe).

The Brand Footprint study, from Kantar’s Worldpanel division, unpacks the 460 billion brand choices made by shoppers last year — an average of 29 brand decisions each month - to reveal the significant headwinds facing FMCG brands. Of all FMCG purchases made in 2023, global brands represented 30% of sales value, unchanged vs 2022. Local and regional brands represented 47% of purchases, while private label sales increased by 0.5 percentage points to reach 22.7%.

Discount retailers achieved 10.5% value growth year on year on a global basis to represent 16% of all grocery spend, compared to 9.6% in 2021. Globally, 61% of households are extremely or very concerned with rising grocery costs. As a result, while 64% of global brands are growing in value terms, only half of FMCG brands are growing in terms of consumer choices – how many times they are chosen off the shelf by consumers.

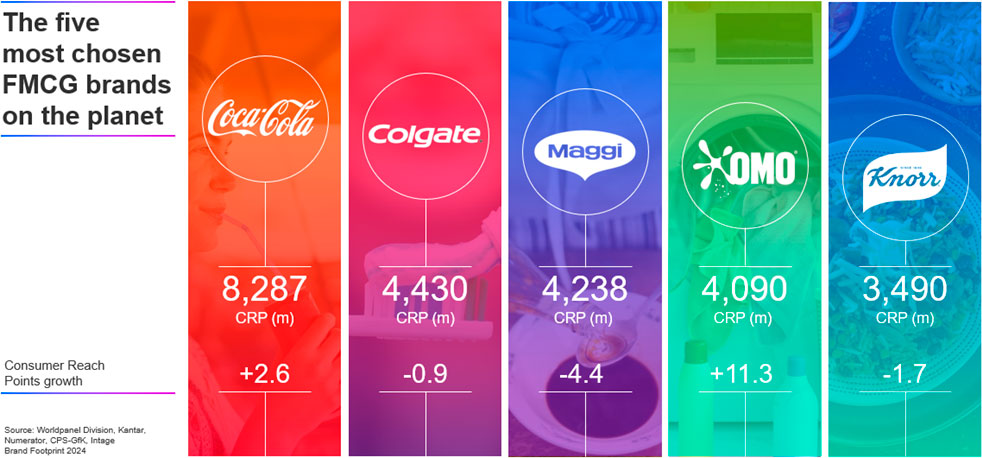

The world’s most chosen brands

Showing the way, the top five most chosen brands in the world are revealed to be Coca-Cola, Colgate, Maggi, OMO and Knorr. Coca-Cola reigns supreme, solidifying its status as the world’s most chosen brand with a staggering 8.3 billion Consumer Reach Points (CRPs). Meanwhile, Colgate sets a benchmark for global penetration, being the only consumer goods brand purchased by over half of the global population, boasting a penetration rate of 55.9%.

Further down the league table, Red Bull emerges as the year’s standout performer. With a 17.8% increase in CRP, it has climbed four spots in the ranking to 20th place, a testament to its growing appeal and strategic market manoeuvres, such as new product development. Purchased by 9.6% of households across the world, it was picked from the shelves 1.4 billion times.

Caffeine-fuelled growth

Analysis of the FMCG categories which are attracting new shoppers reveals a trend in more shoppers buying caffeinated drinks. Instant coffee saw 1.5% penetration growth year on year (purchased by 30.2m shoppers), sports and energy drinks gained 1.2% penetration growth, or 24.3 million shoppers, and carbonated soft drinks gained 1.1% equating to 31.7 million new shoppers.

Guillaume Bacuvier, CEO, Worldpanel Division, Kantar said: “The Brand Footprint 2024 rankings reveal how successful brands have recruited more shoppers in an environment where less costs more and private labels are gaining share. Put simply, they have found ways to be meaningfully different. It’s what happens when brands create strong functional and emotive connections, making the brand mentally available and physically unavoidable, integrating seamlessly across all consumer touchpoints. The brands featured in the report are to be commended for achieving this while pressure on household expenses persists as a stubborn undercurrent in the global economy.”

Access the full Brand Footprint 2024 report.

Explore the rankings of the world’s most chosen FMCG brands.

Watch the webinar to delve deeper into the report’s findings and the winners and the challengers in this dynamic environment.

Contact our experts for further information.