The boost to promotional spending has contributed to bringing inflation down but this isn’t all that’s driving the change. Prices were rising quickly last summer so this latest slowdown is partially down to current figures being compared with those higher rates one year ago.

At the current level of inflation, households would have spent £683 more on their annual grocery bill to buy the same items as they did a year previously, but consumers have adapted their habits to limit this increase. It’s clear that shoppers have dramatically changed their behaviour to combat inflation, whether by trading down to cheaper products or visiting different grocers. The average annual increase to household spending over the past 12 months has actually been £330 – well below the hypothetical £683.

Frequency growth stalls as new habits stick

It also seems the trend towards bigger shops has stuck. We’re visiting the supermarkets less often than we did before the pandemic and buying more when we’re there. Compared to last year, trips to the store have only gone up by 1%. At that rate of change it would take until 2028 for us to get back to 2019 levels. While some people may be shopping less often to manage spending, this is also linked to more people working from home. That has led to fewer opportunities to pop into the shop on the way to or from work. Consumers have been getting into the Wimbledon spirit as the new tennis champions were crowned over the weekend. The first two weeks of July mean strawberry and cream for many and this year didn’t disappoint as record numbers queued to watch the action at SW19. Spending on strawberries and fresh cream shot up by 16% and 13% compared to last year. Shoppers will have been pleased, however, to see that the traditional treat hasn’t hit their pockets too hard this month, with the average price for a pack of strawberries up by just one penny versus last summer.

June saw temperatures soar and consumers took the chance to light up the barbecue. It now seems like a distant memory, but this June was the hottest on record. Plenty of us grabbed the chance to enjoy some outdoor dining with volume sales of barbecue classics like chilled burgers rising by 7% and chilled dips by 5%. Our changeable weather has been less enjoyable for others though and sales of hay fever remedies grew by 16% over the past month as people dealt with seasonal allergies.

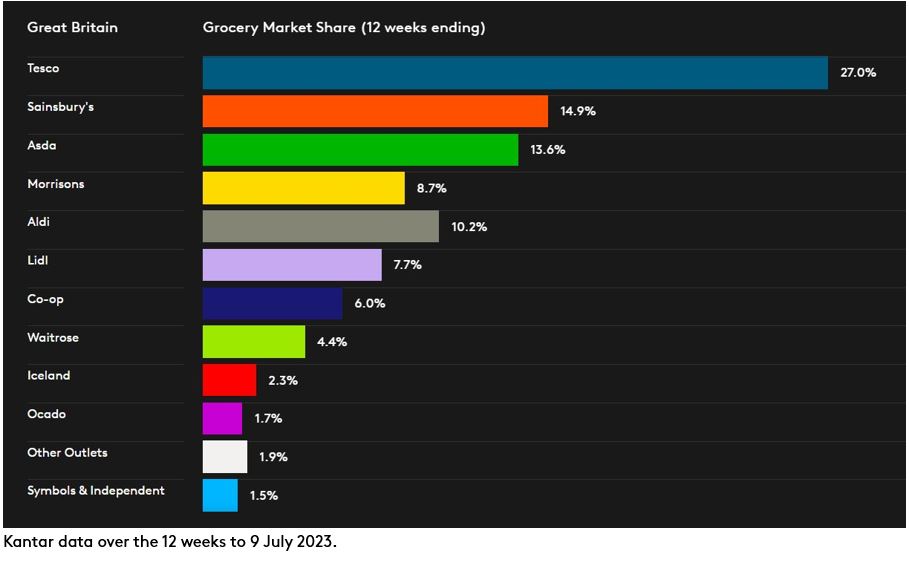

Sainsbury's lead 'big 3' and discounters take more share

Competition for market share among Britain’s three largest retailers remains intense. Sainsbury’s sales growth edged ahead this month, marking the first time since January this year it has led Asda and Tesco. It grew by 10.7%, maintaining its share of the market for the third consecutive month and is now at 14.9%. This was just ahead of Asda and Tesco which increased sales by 10.5% and 10.2%, giving them market shares of 13.6% and 27.0% respectively.

Aldi was again the fastest growing grocer, with sales up by 24.0%. It now holds 10.2% of the market, up from 9.1% a year ago. Lidl increased its market share, up by 0.7 percentage points to 7.7%, with sales increasing by 22.3%.

Morrisons saw growth of 2.5%, its best showing since April 2021 and its eighth month in a row of improved performance. Both Waitrose and Co-op grew by 5.1% over the 12 weeks, the largest boost both retailers have experienced since March 2021. Waitrose now holds 4.4% of the market and Co-op 6.0%.

Iceland maintained a 2.3% share of the market after growing sales by 8.9%. Ocado’s sales rose by 2.0%, taking an overall market share of 1.7%, aided by its much larger 3.0% share in London.