Grocery price inflation fell slightly to 6.8% in January, down from 6.9% in December 2023*, according to our latest data. This softer decline compares with a 2.2 percentage point decrease seen between November and December 2023. Meanwhile, take-home grocery sales grew in value by 2.9% over the four weeks.

All eyes are back on inflation again, after the Consumer Prices Index’s (CPI) unexpected jump earlier in the month. There’s been a lot of speculation about the impact the Red Sea shipping crisis might have on the cost of goods, but the story in the grocery aisles this January is more about the battle between the supermarkets to offer best value, rather than geopolitics. Retailers have taken their foot off the promotions gas slightly as we’ve come into the new year, and that’s meant inflation hasn’t fallen as quickly.

Items bought on offer accounted for 27% of all grocery spending in January versus 32% last month. Christmas is always a bumper period for deals and the grocers pulled the price lever especially hard in December, as they sought to get shoppers through their doors. However, there’s still plenty of opportunities for consumers to make savings. The overall trend in offers is up versus this time last year, and nearly £500 million more was spent on offers this January than in the same month in 2023.

With inflation remaining stubbornly high, Britons are changing their behaviour to better manage their costs. There’s evidence to suggest that people are opting for more homemade meals to keep budgets in line. 86 million more lunchboxes** were made last year, for example. Looking ahead to February, it will be interesting to see how this plays out on Valentine’s Day, and if couples will opt for more low-key celebrations. This was certainly the case in 2023, when we saw a massive £43 million spent on supermarket meal deals costing £10 or more in the week before the special day.

New year, new health

Shoppers have trimmed down in more ways than one this month. As consumers across the country took on Dry January, spending on alcohol fell by more than half compared with December. Almost 6% of beer packs sold this month were no or low-alcohol options, marking a jump from 4% at the end of last year. Sales of own label plant-based ranges increased by 8% on the month, as Veganuary got underway. Health always comes to the fore as a priority for consumers in January, but what’s interesting this month is that we’re not seeing as big a spike in health-related categories as we have done in previous years. That’s because people are now buying more of the typical January ‘health kick’ items throughout the year. 9% of annual own label plant-based sales were made in January in 2023, a steady decline compared with the 11% of sales in 2020.

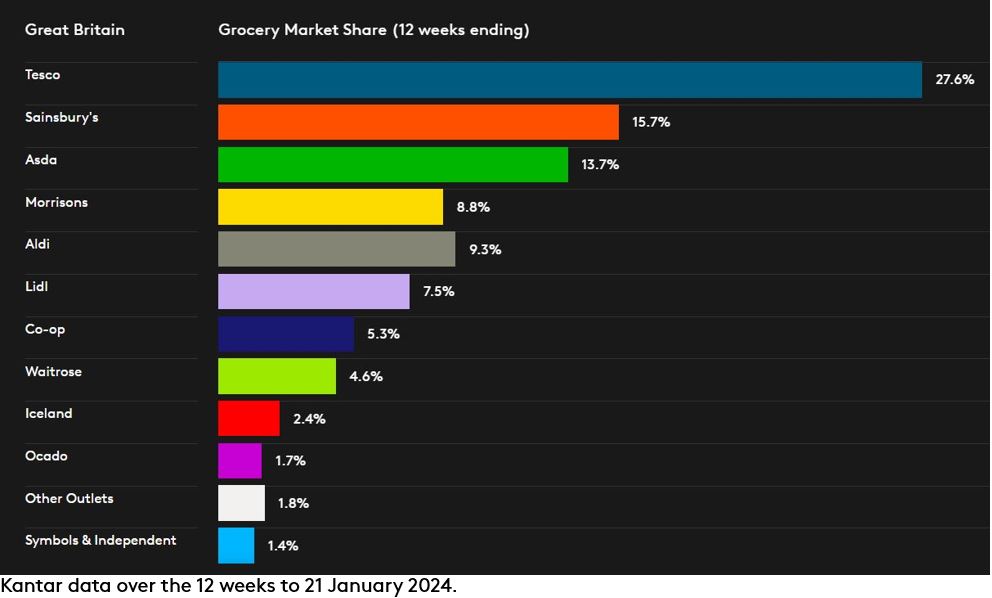

Sainsbury's, Tesco, Lidl and Aldi win share

Both Sainsbury’s and Tesco gained market share over the latest 12 weeks to 21 January 2024 compared with a year ago. Sainsbury’s increased sales by 8.1% to take 15.7% of the market, 0.3 percentage points higher than last year, while the UK’s largest retailer Tesco grew by 6.3% and now has a share of 27.6%, up from 27.5%.

Lidl was the fastest growing grocer in Britain for the fifth month in row and the only retailer to see double-digit growth in the latest 12 weeks. Spending at the discounter was up by 11.9%, bringing its share of the market to 7.5%. Aldi also grew ahead of the market, with sales up by 7.2%, and increased its share by 0.1 percentage points to 9.3%.

Sales at Morrisons rose by 2.8%, with the Bradford-based grocer now holding an 8.8% share. Asda’s share is at 13.7%, with sales rising by 2.1% compared to a year ago.

Waitrose increased sales by 3.5% and holds 4.6% of the market, while Co-op accounts for 5.3%, growing sales by 1.8%. Iceland saw growth of 2.3%, giving the frozen food specialist a 2.4% share.

Online sales rose by 6.3% in the latest 12 weeks, slightly ahead of Ocado’s growth where spending was 4.0% higher than last year. The online-only retailer has a 1.7% share of the total market.

*With additional information becoming available, Kantar has re-stated the level of like-for-like grocery inflation during the four weeks ending 24 Dec 2023 as 6.9%, versus the 6.7% previously communicated. The marginal re-statement does not affect conclusions drawn from the data in the previous Grocery Market Share press release, nor does it have any impact on the Till Roll growth rates or market shares for any retailer. We are drawing this change to your attention as the grocery inflation rate in the latest four weeks ending 21 Jan 2024 of 6.8% should be compared with the re-stated 6.9%, thus showing a fall in inflation.

**This data has been sourced from Kantar Worldpanel’s Usage panel, for the 52 weeks ending 24 December 2023.