2021 was the year we began to emerge from the pandemic, but not from the crisis it helped to cause. New pressures continue to add up for the Latin American consumer in 2022. Shoppers have been going through a process of reinvention, visiting more channels to buy FMCG than ever before and being cautious with their pockets in an attempt to beat inflation.

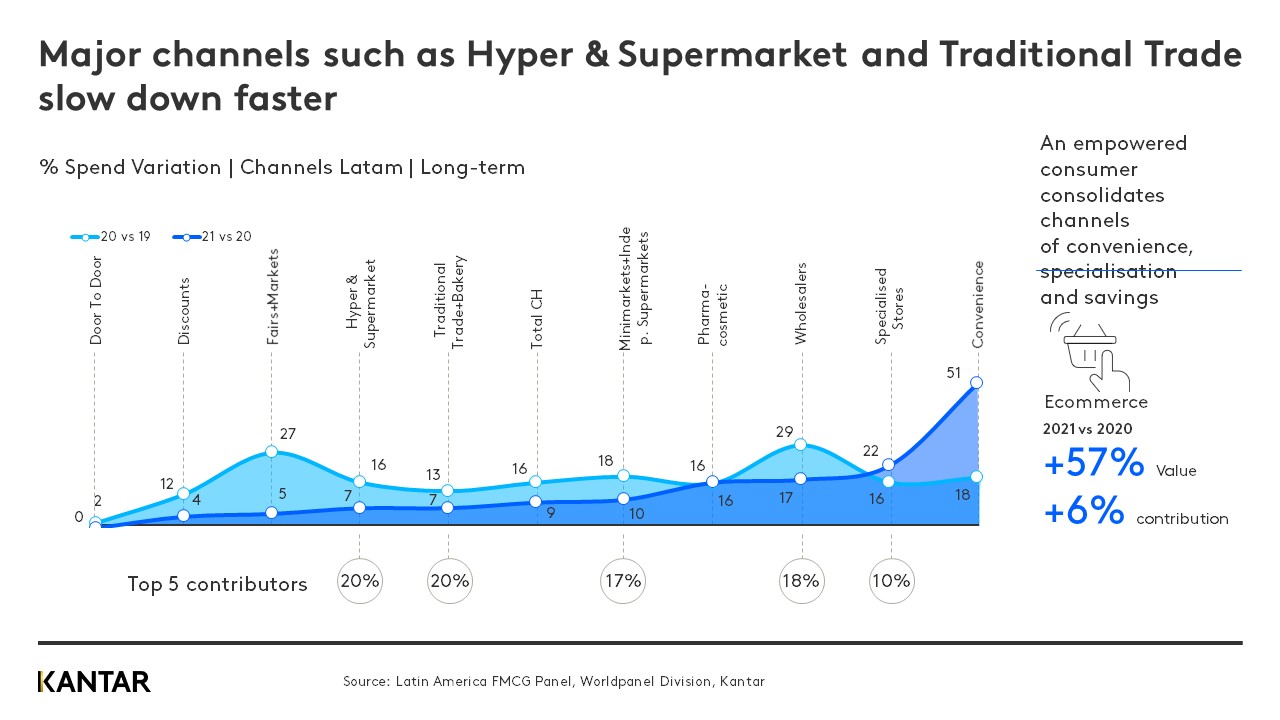

The pace of growth within FMCG channels is nuanced. New ones are standing out, with wholesalers, pharmacies, specialist stores and convenience stores leading in terms of spend. Meanwhile value growth in hypermarkets, supermarkets and traditional trade is decelerating fast. All of these trends are being driven by shoppers’ demands for value for money, convenience and specialization.

Digitalization is the main takeaway from the pandemic

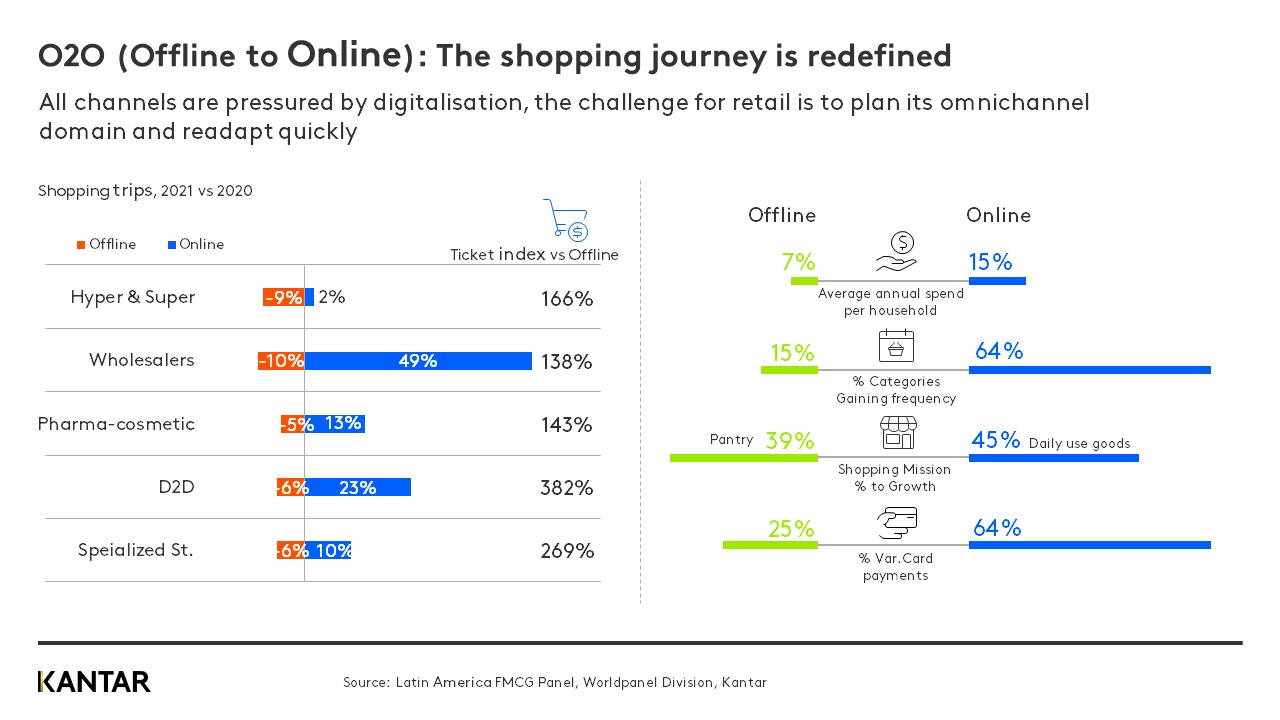

On average, household spending on FMCG in Latin America increased by 26% between 2021 and 2019. The main pillar of this trend is 'phygital' behavior – a mix between physical and digital purchasing. The growing number of different digital outlets has allowed FMCG brands to increase their exposure. In 2021, more households in Latam purchased FMCG products online than ever before. Penetration is highest in Argentina at 39%, a rise of 12% compared with 2020, followed by Chile (38%) and Bolivia (35%). But if we look closely, we see that growth has dropped from triple to single digits, and is starting to be driven by greater loyalty – a sign that early ecommerce adopters have already entered another stage of their relationship with the channel.

A new concept is also emerging that will set the tone for the coming years. O2O (offline to online) spend is growing as shoppers migrate to digital channels that offer a better experience compared to in-store encounters, with greater fluidity and speed of service. The level of cross-platform interactions – which involve both digital and physical activity – has increased by 18% compared with 2019, and spending in Latin America has become more fragmented as a result.

Who is the omnichannel shopper?

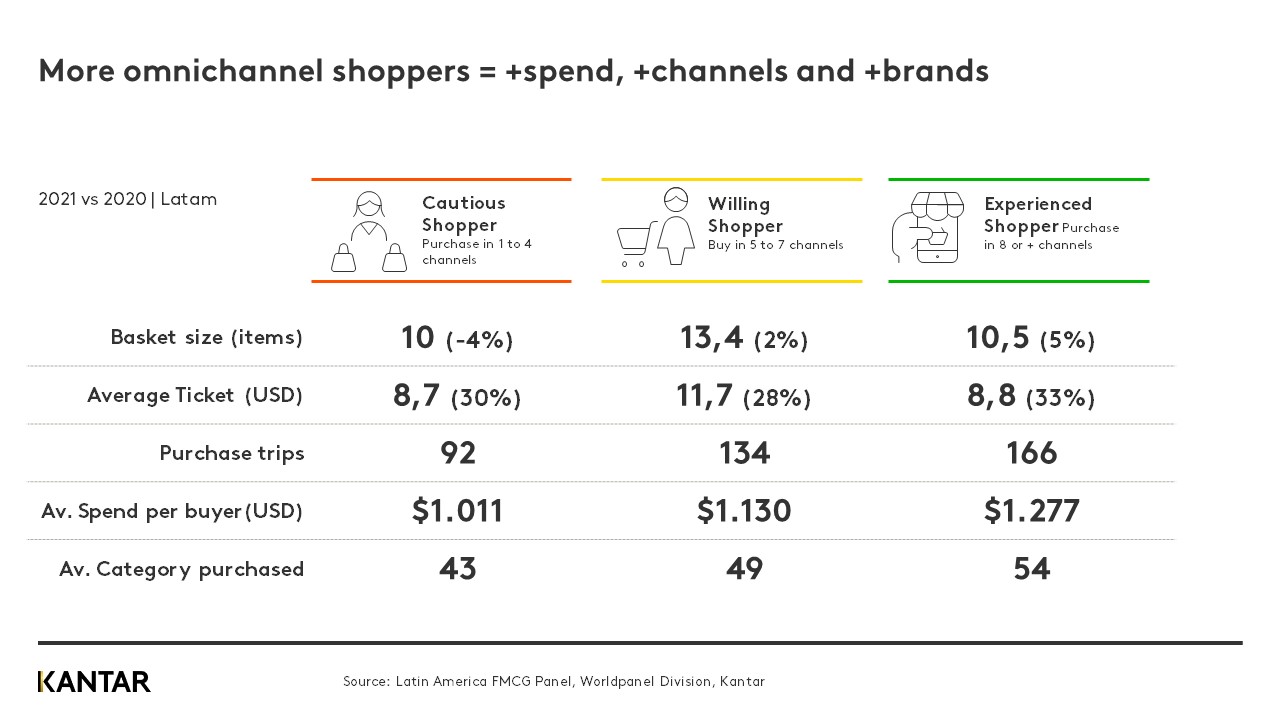

Segmenting Latin shoppers according to the number of channels they visit, we can identify three main groups:

- Cautious shoppers, who visit from 1 to 4 channels a year

- Willing shoppers, who visit on average 5-7 channels, and finally

- Experienced shoppers, who visit 8 or more channels annually.

The Experienced shopper has the most contact with points of sale, with a purchase frequency of 166 times a year, and also spends the most on their FMCG basket – 26% more than the Cautious shopper. Even more significant, this is the group that buys the highest number of categories, providing more brands with the opportunity to play.

It is time for both manufacturers and retail channels to work together to design and implement an effective omnichannel strategy that aligns with the personality of today's Latam shopper. Knowing what differentiates the dynamics of the physical and digital worlds, and how to play with the right product in the right channel, will be essential for achieving growth.

As mentioned, the most important FMCG channels are already experiencing value growth below the level they reached in 2021. In this environment of change and upheaval, it’s vital to understand the shopper's journey in order to better capitalize on each step and identify the best strategy for each type of channel.

We can help you put the shopper at the center of the FMCG consumption equation by understanding the market’s short-term dynamics, so you can succeed in uncertain times. Talk to our expert team now about how to manage and evolve your offer.