Grocery price inflation fell by 2.2 percentage points to 12.7% in the four weeks to 6 August 2023, according to our latest data. Overall take-home grocery sales increased by 6.5% over the same period, down from 10.4% last month.

The latest slowdown in price rises is the second sharpest monthly fall since we started monitoring grocery inflation in this way back in 2008. Prices are still up year-on-year across every supermarket shelf, but consumers will have been relieved to see the cost of some staple goods starting to edge down compared with earlier in 2023. Shoppers paid £1.50 for four pints of milk last month, down from £1.69 in March, while the average cost of a litre of sunflower oil is now £2.19, 22 pence less than in the spring.

Shopper trading down to avoid half of inflationary hit

Own-label goods remained popular in the latest four-week period, with sales up by 9.7%, while branded products rose by 6.4%. Own-label sales continue to outpace branded, although the gap between the two is closing. Buying supermarket lines is just one of the ways people have been trying to save money at the tills and we can see the impact on how much they are spending. The average increase in households’ weekly grocery shop is £5.13 compared with last year, well below the £11.27 extra they would have paid if consumers had bought exactly the same items as 12 months ago based on the current rate of inflation.

While consumers grapple with price rises, retailers beyond the supermarkets are also battling to maintain their position on the high street, with news of Wilko falling into administration signalling the extent of the challenges some businesses are facing. Wilko is a popular choice for many shoppers with 7.6 million households visiting its stores to buy groceries in the last year. Grocery items make up just under half of its sales, with homeware at 15%, DIY at 9% and garden products at 7%*. Wilko’s rivals will be keeping a close eye on its fortunes in the coming days and weeks as they look to draw some of its shoppers through their doors.

Damp summer hits footfall but boosts warming foods

Hopes of some sunshine were dashed this July as unseasonable weather put the dampeners on sales of our usual summer favourites. It was a better month for Barbie than barbecues this July as the rain put a spanner in the works for many consumers’ outdoor plans – a stark comparison to last year when we experienced the hottest day on record. Volume sales of ice creams were down by 30%, while soft drinks sales were nearly a fifth lower than 12 months ago. Halloumi, a new staple of the British summer menu with shopper numbers growing by 218% since a decade ago, was also down by 27%.

Instead of our usual summer fare, it seems we’ve been turning to more traditional winter warmers instead. The amount of soup bought has gone up by 16% year on year, while roasting joints have grown by 5%. Cooler temperatures and a wetter than average month may have also put people off from venturing to the shops. Footfall was down for the first time in 18 months with people making 320,000 fewer trips to physical supermarkets than a year ago.

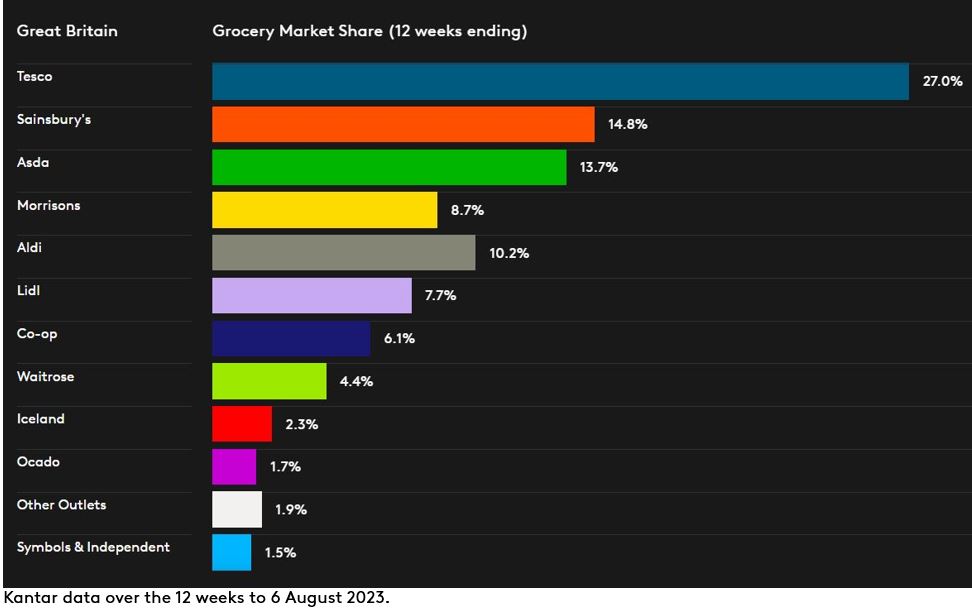

Both Tesco and Sainsbury’s outperformed the market this month, fuelled by sales growth of 9.5% and 9.3% respectively over the 12 weeks to 6 August. Tesco boosted its market share to 27.0%, from 26.9% a year ago, and Sainsbury’s held firm year on year at 14.8%. Asda pushed its sales up by 7.7% this month and now accounts for 13.7% of the market, while Morrisons has an 8.7% share as sales grew 2.3% compared with last year.

Aldi was the fastest growing retailer for the fourth month in a row, with sales increasing by 21.2% versus 2022. The discounter now has a market share of 10.2%, a rise of 1.1 percentage points year on year. Lidl’s sales rose by 19.8% and the retailer now holds 7.7% of the market.

Sales at Waitrose and Co-op rose by 4.4% and 3.4%, giving the retailers market shares of 4.4% and 6.1%. Frozen food specialist Iceland saw sales increase by 6.7% to take a 2.3% share, while Ocado’s share now stands at 1.7% as spending at the online-only retailer grew by 1.4%.

*Worldpanel Plus 52w/e 9 July 2023