Due to the COVID-19 pandemic, Vietnam’s economic growth slowed to +3.82% in the first quarter of 2020. The average price of a basket of consumer goods on the other hand increased by 5.56% – the highest rate in the last seven years.

The good news is that the battle against COVID-19 in Vietnam has eased up, but it is not over yet. As its final impact on the economy and businesses is difficult to predict entirely, the expectation is that the country will face challenges at least until July. As a result, Vietnam’s full-year GDP growth is forecast to be about 5%, which is lower than expected.

Similar to the experience in China, the COVID-19 crisis will likely pivot through different phases as the situation develops. It’s important to understand the impact through each phase in order to respond, prepare, and predict the future.

The following analysis focuses on the first eight weeks of the pandemic, ending 22nd March which is before the national social distancing order became effective on 1 April, which is defined as the ‘pre-lockdown period’.

Behavioural changes potentially shape new habits

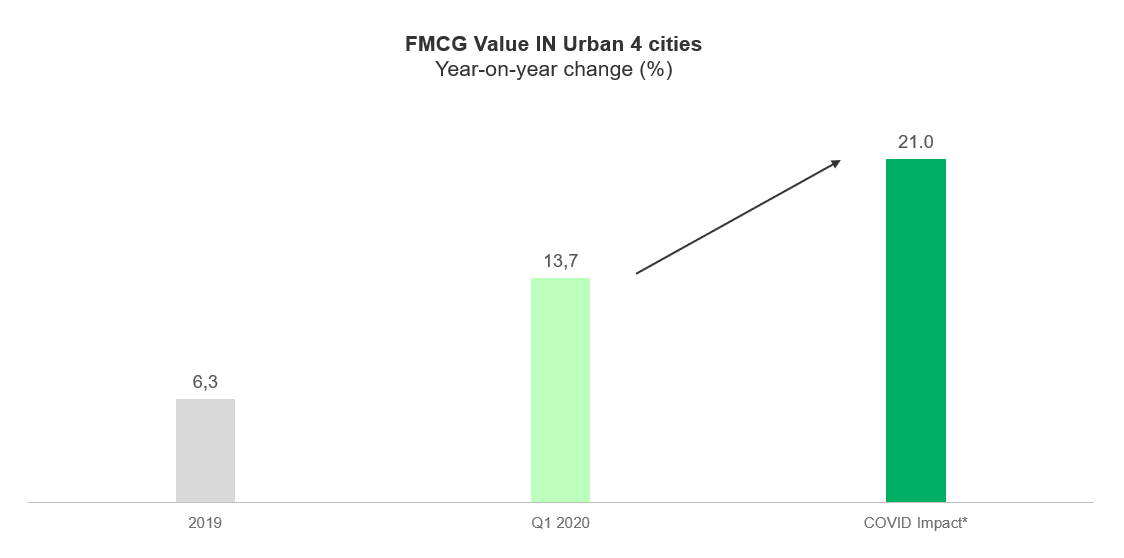

At the first stage of pre-lockdown, Vietnamese consumers cut down spend in some areas such as out of home activities and luxury items. They shifted their focus to staple needs including fresh food and essential packaged consumer goods to survive during the self-isolation time. Consumer spend on FMCG picked up strongly in the first quarter of 2020, hitting double-digit growth. The abnormal spike was over the first eight weeks of COVID-19, especially in big cities. This indicates some degree of stock-up behaviour among Vietnamese consumers as social distancing was enforced to avoid exposure. While it may not be the same for all categories in FMCG, we expect the market to return to its “single-digit growth” when the pandemic is over.

[COVID impact*: The first eight weeks of COVID-19 – 8 weeks ending 22nd March 2020 compared to an equivalent period of eight weeks last year – eight weeks ending 31 March 2019]

Changes in shopping behaviour differ by region. Due to the availability of big retail formats, urban consumers made bigger shopping trips with more items to limit travel and contact. In rural areas, where traditional channels remain key, consumers made more trips.

Moving towards the second stage, national lockdown will likely result in the further reduction of shopping frequency given restrictive shopping and transportation, while the basket size might significantly increase.

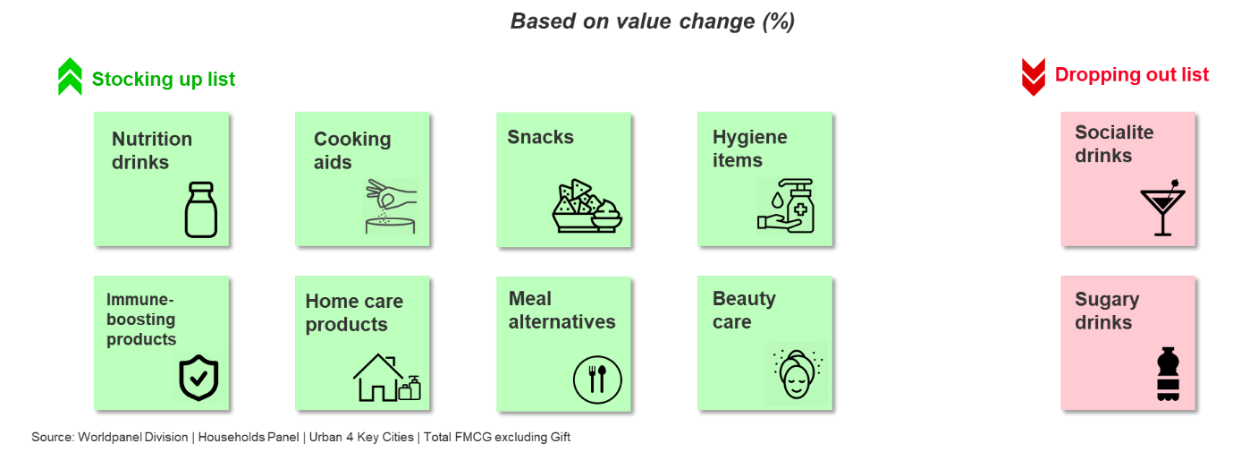

Consumers focused on four key buckets of categories at this time showing an increased preference for essentials, convenience foods, health-boosting and hygiene products. Besides health and hygiene products, the upsurge of cooking aids, snacks and meal replacements are demonstrating new habits potentially formed as a result of more time spent indoors. The lockdown period, which means more time at home, will probably generate new routines and choices which will influence future demand. It will be interesting to understand how consumers feel about these changes in order to assess the potential impact in the coming months, for example whether these increases are purchases brought forward, or if there will be increases in consumption in the long term.

Noticeably, some areas of beauty care, particularly the skincare segment, have sustained growth thanks to flexitime under the “stay home” campaigns. This trend is the opposite to what happened in developed countries like China and European markets where there are fewer personal care occasions because of working from home. It could be explained by the fact that makeup is still underdeveloped in Vietnam with its immature reach of just a quarter of urban housewives. Hence, there is a small difference between usage whether people stay at home or go out to work. Yet, in the following phase of COVID-19, we may expect some impact on the beauty sector due to store closures and more limited product availability, as the country moves to quarantine and lockdown mode.

Beverages continued to struggle in March. Enjoyment drinks and sugary drinks are the most heavily affected categories amid the pandemic, such as beer, carbonated soft drinks and ready-to-drink tea. However, we start to see several actions taken from brands in order to recover. Embracing digital seems the most relevant and common way to deal with the situation. In China one-third of consumers used delivery/O2O (online to offline) services to order milk or herbal tea online during the month after the COVID-19 outbreak. Moving to online and offering doorstep delivery could be one step to turn things around or at least to help minimize the loss.

Channel dynamics to rethink retail strategy

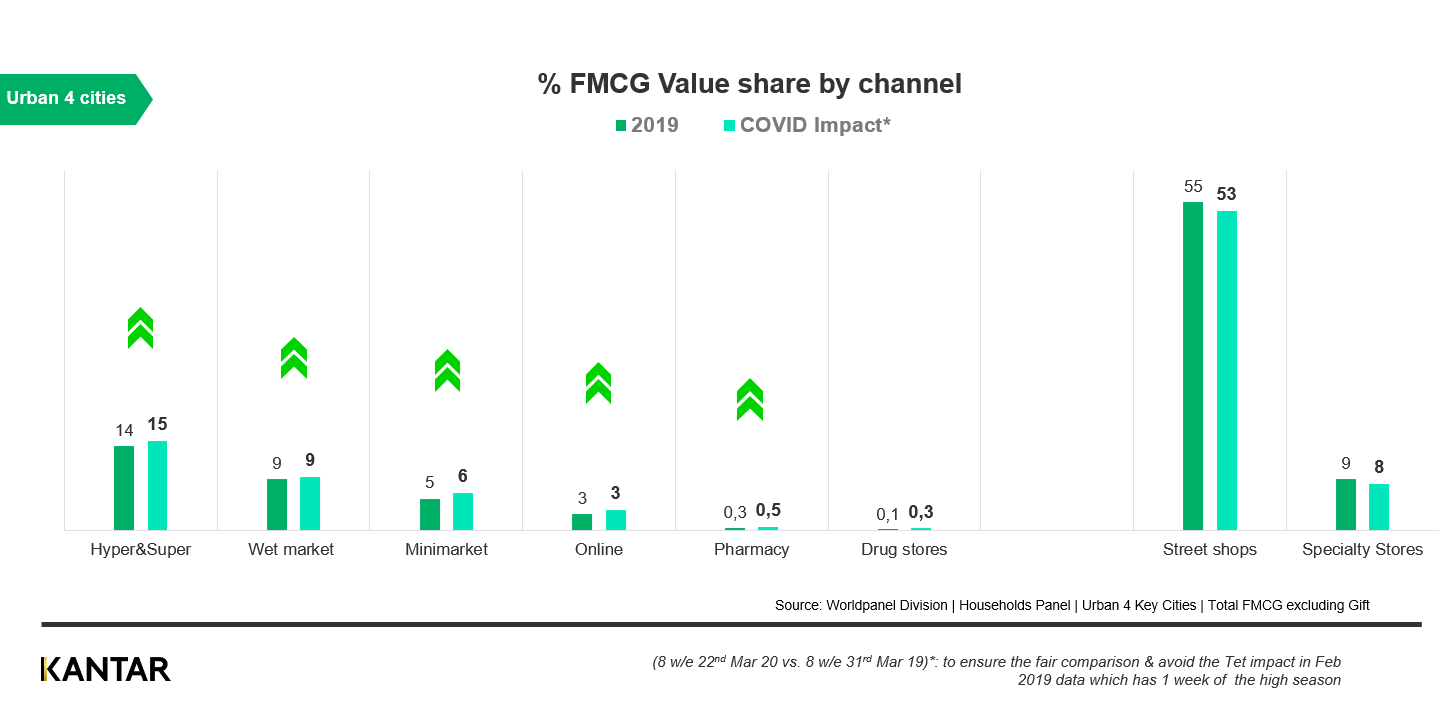

With the concern of infection, we have seen an impact on the way people shop. Interestingly, all channels have been achieving double-digit growth, which has never been seen over the past seven years. It implies that the omnichannel shopping trend is stronger during the pandemic. Different channels serve different consumer needs. To stock-up, consumers go shopping at the hypermarket or supermarket and emerging channels such as online while they use the minimarket more frequently and buy more in traditional channels like street shops and wet markets.

Big modern formats (including hypermarkets, supermarkets and even cash & carry) and emerging formats have outpaced traditional trade during this uncertain time. In the context of COVID-19, listing a wide variety of categories, brands and pack sizes can help to attract shoppers to the store, as they are confident that they can get everything they need, especially fresh food. This is a key advantage of big retail formats, in turn driving the increase in footfall. Consumers currently visit hypermarkets and supermarkets more often than ever before, with a purchase on average made every 10 days to the four weeks ending 22nd March. COVID-19 has pushed Vietnamese people to try new things. There are a significant number of consumers who haven’t shopped FMCG products online or at minimarkets before, now starting to make their first transactions. Consequently, both online shopping and the minimart format reached a peak in terms of shopper base versus any historical four-week period. Though these channels had already shown good progress in Vietnam over recent years, it presents a chance for them to further expand if new shoppers enjoyed their experience. Understanding this and working to remove other existing barriers will be key for the continued development of these emerging channels after the crisis.

Big C, Bach Hoa Xanh and Mega Market are physical retailers managing to achieve an impressive surge during pre-lockdown. In terms of online shopping, incremental FMCG transactions came from both social commerce and ecommerce. Facebook - the most popular social media platform - remains the most chosen platform for online FMCG purchases, followed by Shopee - the pure ecommerce player. Both of them recorded triple-digit growth.

While some of these changes and winners may be short-term, there will be many hoping to extend this opportunity into the long term, pointing to how we may behave in the next phases of COVID-19. The implications for FMCG players will be to re-think and develop growth strategies and partnerships with the key retailers in order to win the “new normal”.

Contact us or get in touch with your usual contacts at Kantar to discuss what we can support you to navigate the uncertainty.