The January 2026 results of the UK Customer Satisfaction Index are in, and the banking sector has achieved its highest ever scores1. We might presume this is the result of the influx of digital challengers to the category. Possibly. But the two banks that make the overall top five rankings are First Direct, at number one, and Nationwide Building Society, in fourth. They are not fintechs, they are two banks that pride themselves on their people-centric approach to customer service: First Direct, renowned for their quick-answering telephone contact centre, and Nationwide, with their commitment to keep their branches open until 2030.

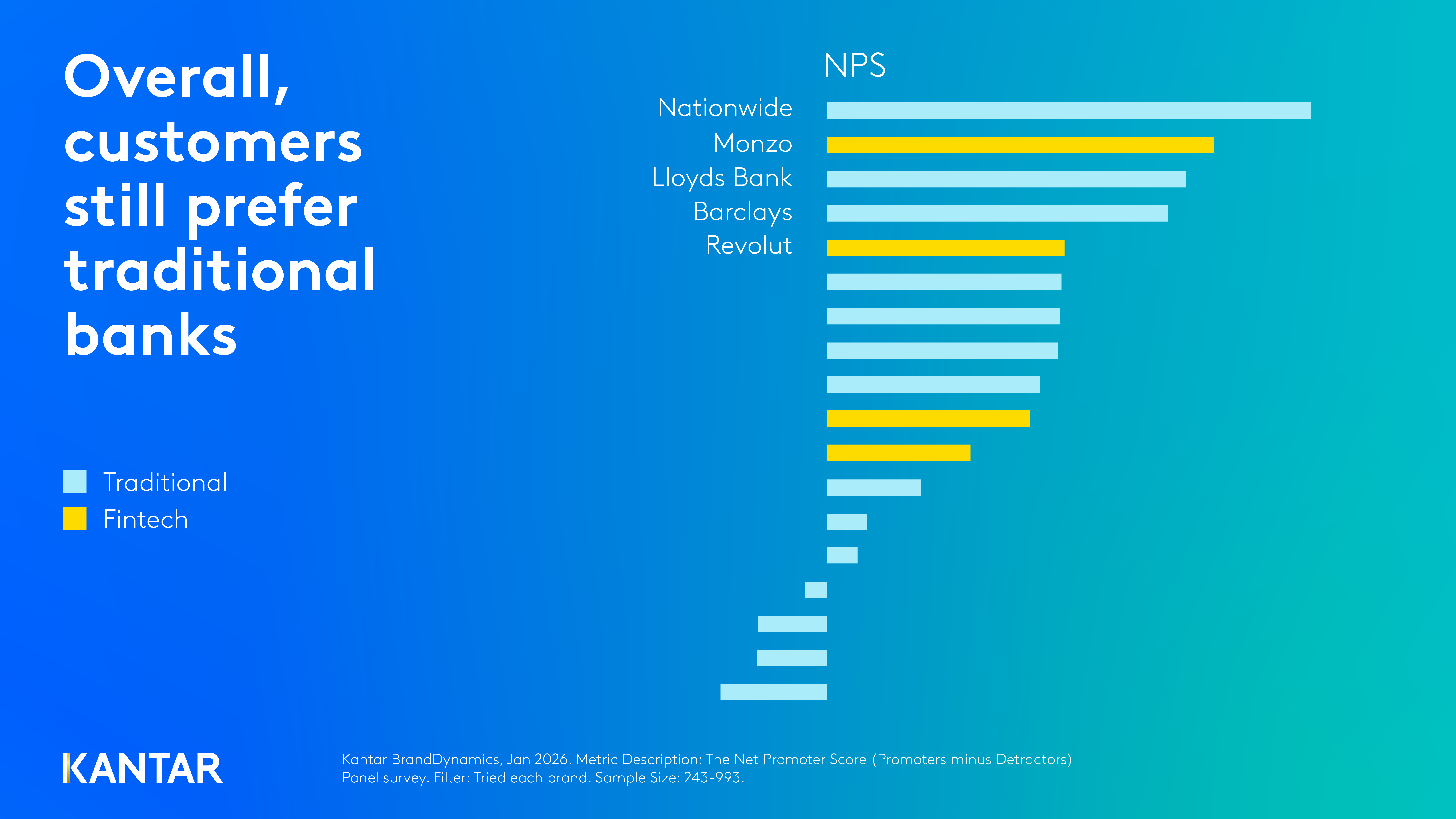

While a great digital-first experience is one of the most important aspects of banking, customers still, overall, prefer banking with traditional players. Our ongoing Kantar BrandDynamics tracking of customer perceptions for 18 major UK banks shows that for customers’ likelihood to recommend, in January 2026 the top ranked brand was Nationwide. And the fintechs? Monzo leads in second, with Revolut fifth, and Starling 11th2. Good, but not experience leaders. It raises the question: are fintechs more sparkle than substance?

Many people bank with both traditional players and fintechs. So, what happens when you make the switch? How does the shiny new fintech account make you feel about your old bank?

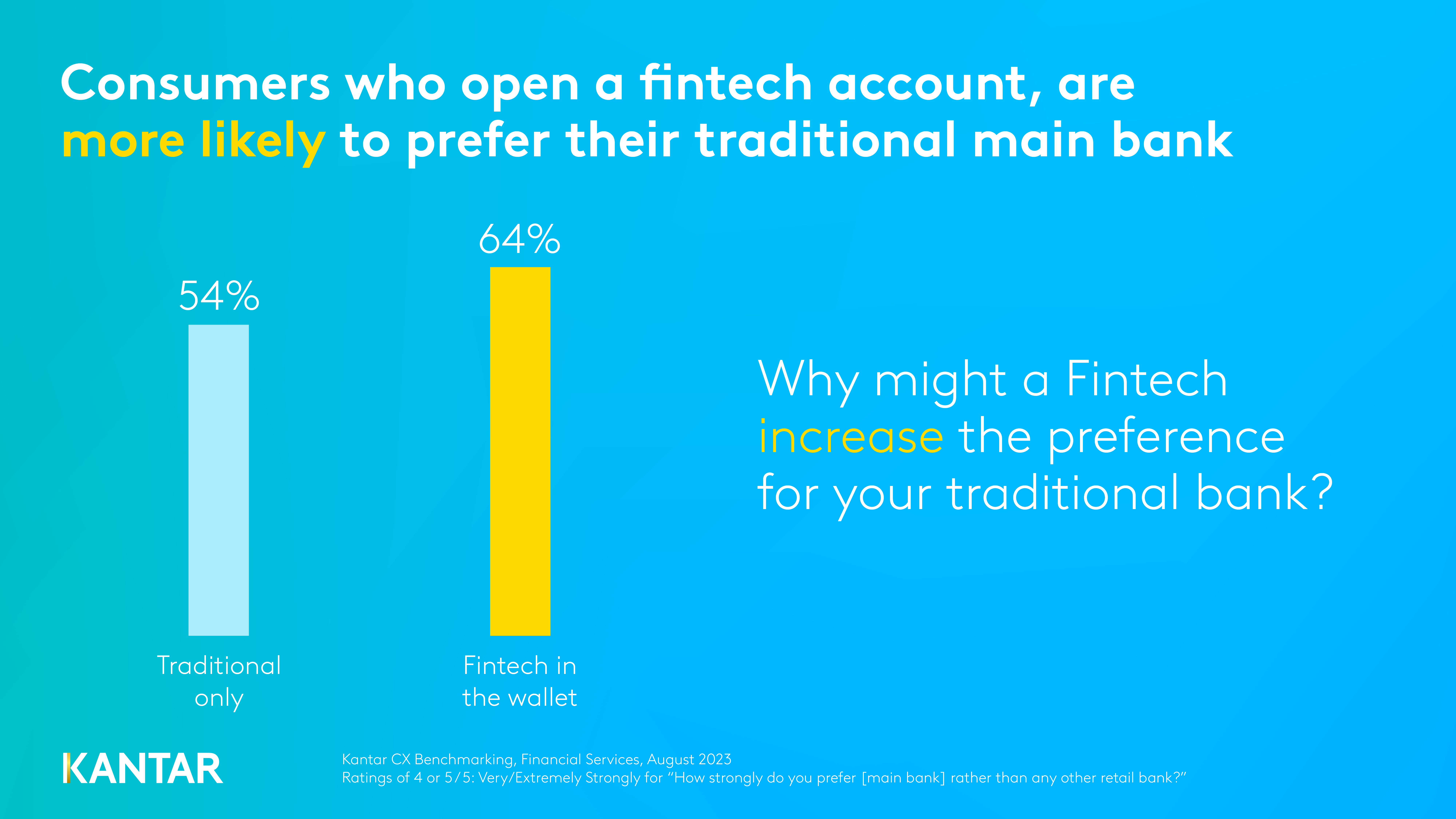

We found that consumers who open an account with a fintech are more likely to prefer their existing traditional bank. These ‘fintech customers’ give higher preference scores for their traditional, main bank than those who only bank with established players3. Surely exposure to slick fintech apps would erode loyalty to legacy banks? And yet, the opposite appears true.

This gets to the heart of what consumers want from their banks, and how different providers fill increasingly specific roles in people’s lives.

Love the one you’re with

Enter the Lamborghini Paradox. Maybe, everyone would love a Lamborghini. It would look lovely on the drive. People might smile, even point, when you take it out. But then reality hits: potholes, speed bumps, multi-storey car parks with tight spaces. Two kids and nowhere to put the shopping. You'd miss your sensible Volvo. How often do you need to go from 0-60 in under three seconds anyway?

Similarly, fintechs are beautifully designed, with market leading tech and innovative features. The cards look great when you take them out. They are perfect for payments. But for the full range of life's financial needs, customers still want the reliability of traditional bank. The digital experience needs to be good, but people also want to know that someone will answer the phone when something odd shows up on their statement. Life is full of potholes.

Sparkly new things

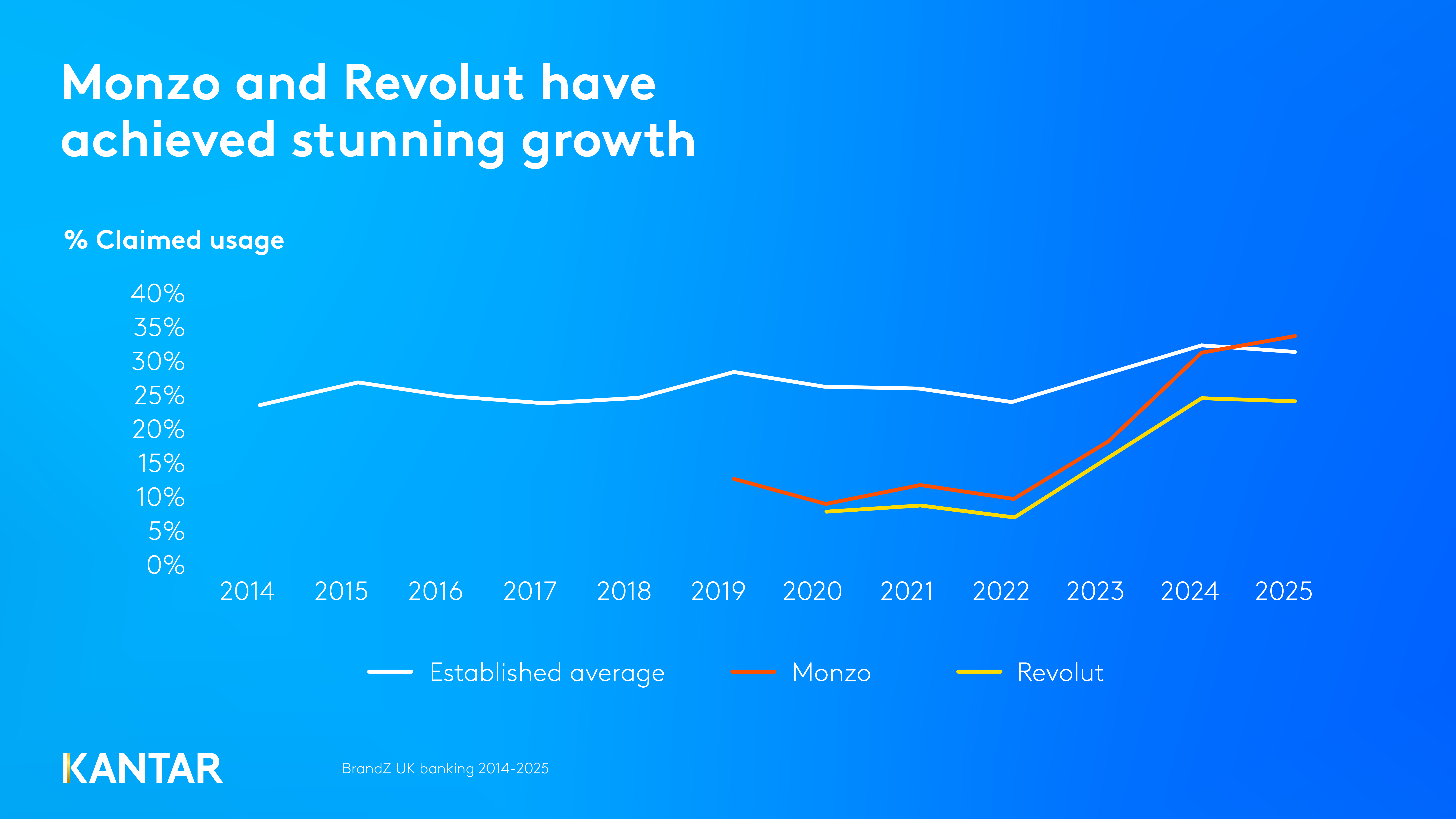

The scale of fintech growth is undeniable. Monzo's claimed usage has grown from 7% to 34% between 2020 and 2025, while Revolut has climbed from 5% to 24%.4 People are adding fintechs to their ‘banking repertoire’ in great numbers.

The fintechs are perceived as new and ‘different’, which has propelled their growth. Standing out as unique is the leading predictor of future growth5. It gets you noticed and attracts people to your brand. When comparing scores for ‘difference’ of banks in 2023, Kantar BrandDynamics data revealed those with the most difference grew four times more than those with low difference over the next two years. Back in 2023, who were the most ‘different’ banks? Monzo, Chase, Revolut and Starling. All fintechs, with Chase entering the UK market as a digital-only bank.

Consumers often open an account with a fintech for a specific purpose, like going on holiday and looking for interest-free foreign transactions6. But people rarely switch all their finances to the fintech. Instead, they are opened alongside as an additional provider. This is reflected in the overall decline in year on year switching between 2023 and 2025, with comparatively small numbers switching their salary and direct debits to Monzo, or any other fintech7.

But when the holiday ends? Most people go back to their old banks. Sure, you might use the fintech every day for coffee, commuting, and online shopping. But it doesn’t feel like the primary banking relationship, where your salary gets paid in, or where you have your savings, or a loan.

We see this when asking customers which bank is the one they use the most. Even though similar numbers of customers claim to use NatWest as claim to use Monzo, the depth of usage is very different; 53% of NatWest customers say NatWest is their most used, compared to just 37% of Monzo customers saying Monzo2.

This strength of presence in the wallet makes the established banks still the first choice for most consumers when opening new products. The top five banks in January 2026 that customers most recently opened new accounts with are Barclays, Nationwide, Lloyds Bank, Halifax and NatWest. Monzo are seventh and Revolut are ninth2.

When you return from holiday, normal life resumes.

The novelty wears off

One of the biggest impacts of the fintechs is creating competition in the category, raising consumer expectations, and pushing the established banks to up their digital game.

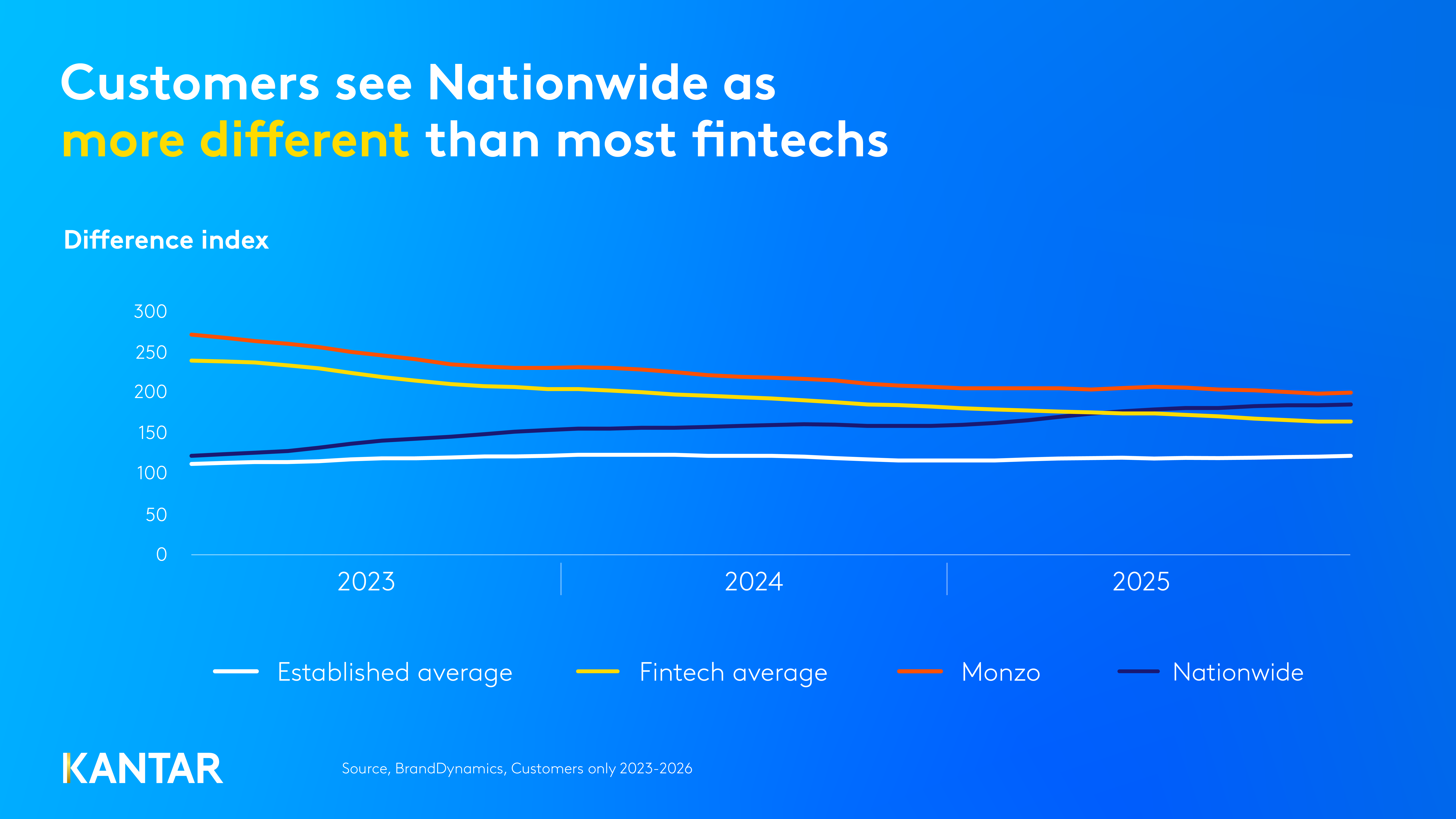

As established banks have improved their digital offerings, the perceived difference gap has narrowed2. Established banks have all increased in perceptions of difference, while fintechs have declined. Among their customers, Monzo still scores highest for difference in 2025, but number two? Nationwide, a 140-year-old British building society, a bank owned by its customers (or ‘members’).

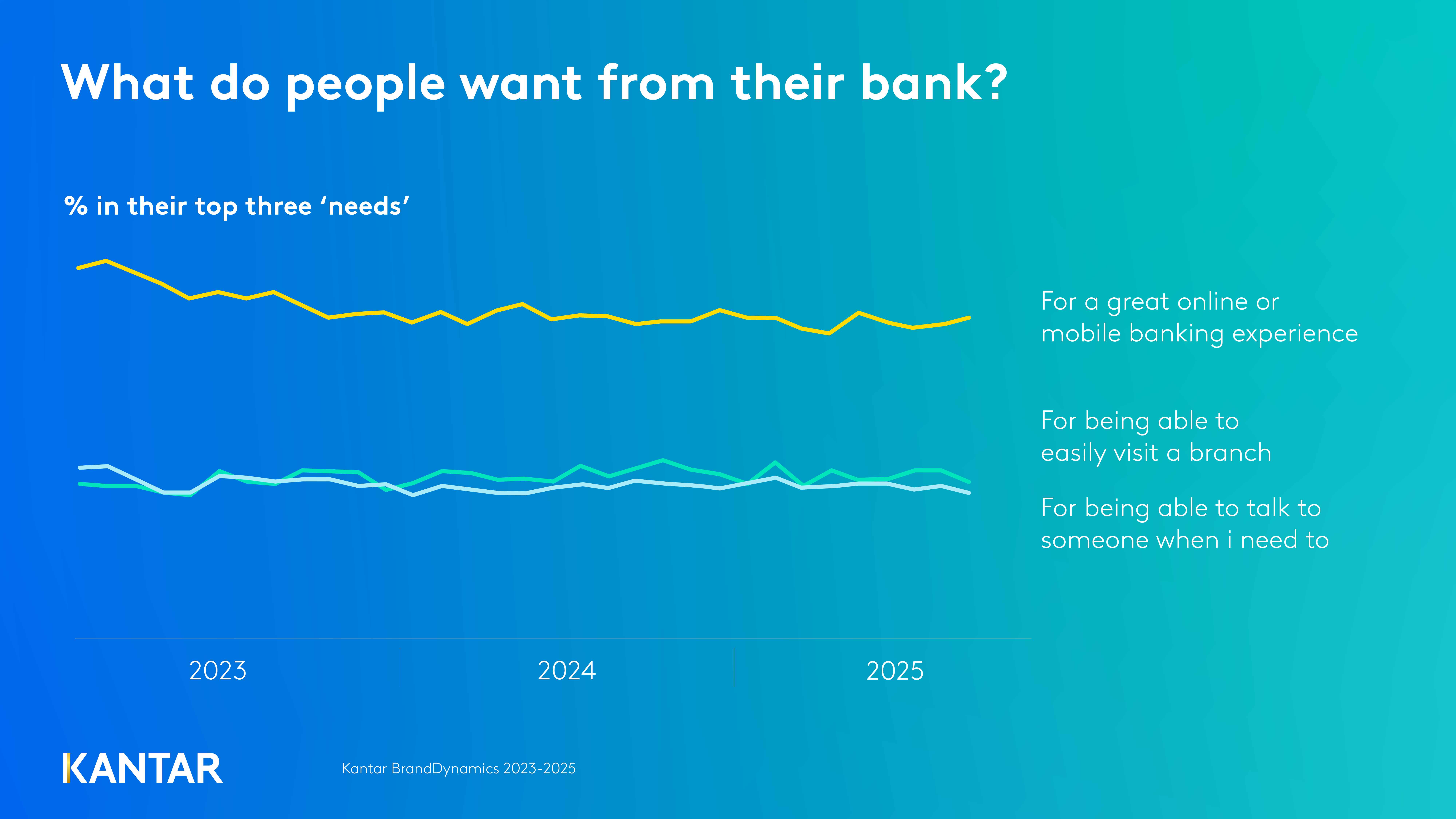

Even with such an increase in fintech adoption, the need for human interaction, or to access a branch if needed has remained stable over the past two years. The need for a great digital banking experience remains high but has dropped slightly over this time2.

This demonstrates that offering a great digital experience remains very important, but customers still need to feel reassured that human support is available. People still want the services offered by banks like First Direct and Nationwide.

Go your own way

Monzo and Nationwide are the only two UK banks to appear in the FT/The Banker's "Banks with Momentum" list, powered by Kantar analysis, which identifies the top 50 banks across the world most likely to grow over the next year8.

What's striking is how Monzo and Nationwide have each achieved their success. One is a digital-first fintech. The other has committed to keep their branches open until 2030, while competitors are closing theirs.

Nationwide has doubled down on human connection. They've linked their annual £100 ‘Fairer Share’ member payment not just to a financial benefit, but to their core identity as a member-owned organisation. Their message to customers: “We’re a good way to bank”.

Nationwide are number one in perceptions of caring for their customers, affinity (or ‘brand love’), and overall trust2. Everything they do emphasises that “we're different because we belong to you”. They recognise that customers still need the reassurance of a branch and a good contact centre. Nationwide’s promise of “Banking – but fairer, more rewarding, and for the good of society” recognises that consumers still seek brands that provide a positive, supportive presence in the community. This is a powerful way to tap into broader societal sentiments while being true to your purpose, and it works.

Monzo, on the other hand, has pursued digital excellence relentlessly. Their experience is effortless, their brand positioning clear: "Money never felt so Monzo." Monzo are perceived as number one for 'setting the trends' in banking.

If Monzo could offer the full gamut of banking services, would they dominate the market? Potentially. Right now, they are expanding their range of services, including more profitable areas. In December 2025, Monzo announced the acquisition of Habito, a digital mortgage broker. “We're excited to bring Monzo's simplicity and transparency to one of life's biggest financial moments." said Kunal Malani, Chief Banking Officer at Monzo. Simplifying the home buying process and making mortgage over-payments easier are two ‘needs’ where Monzo hope to lead the way. They also provide an aggregation service to see all your financial products and pensions in the app, and wider savings and investments offerings, including Monzo Pots for savings, plus Stocks and Shares ISAs and Exchange Traded Funds.

Customers have a range of needs for banking products. Both Monzo and Nationwide recognise that they must deliver and be front of mind for as many of these needs as possible, providing a service that is both functionally and emotionally differentiated.

Marketing and customer experience leaders must think a little less Lamborghini and a little more Volvo: Avoid being distracted by shiny technology or the assumption that customer needs have fundamentally changed. They haven't. Technology rather creates the opportunity to help customers service these needs a little better, and glide over the potholes of life.

The winning approach is to understand what your customers truly need and deliver it in a way that only you can.

Get in touch

Watch a short demo on how you can measure and improve the impact of your customer experience with ExperienceEvaluator.

Go deeper

Read how a clear sense of difference is vital for creating momentum for growth in banking

Discover how Nationwide and Kantar delivered insight-led CX transformation in our recent webinar

Read Kantar's latest research across five markets and multiple sectors, revealing why brands that focus on unique experiences are the ones that truly drive growth: When Good Isn’t Good Enough: Rethinking CX for Brand Growth

Sources & references

1 Institute of Customer Service, 2026

2 Kantar BrandDynamics, 2022-2026

3 Kantar Retail Banking Benchmarking, 2023

4 Kantar BrandZ, 2020-2025

5 Kantar Blueprint for Brand Growth, 2025

6 Kantar Digital Analytics 2024

8 The Banker, On Brand: The 50 fastest growing banks, 2025