In Vietnam, the first official announcement of COVID-19 in the country was on 1 February. It has now moved into the second phase of the outbreak, with the seventeenth case recently reported. Prior to the pandemic, hopes for 2020 were that the country would maintain and continue the strong GDP growth of 7.02% in 2019; however, this is now looking less achievable.

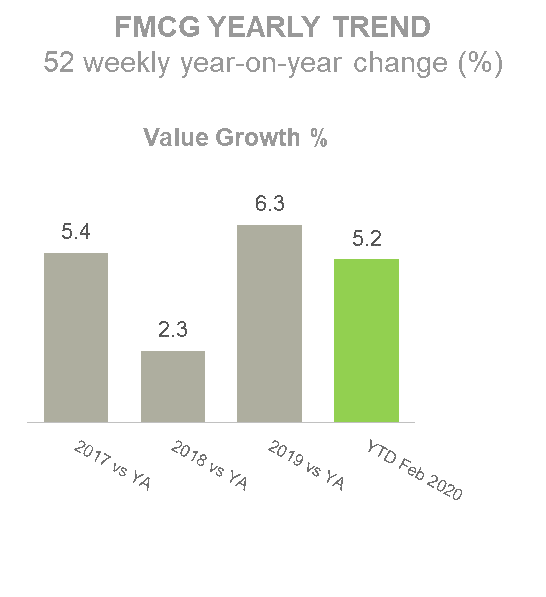

In the first two months of 2020, inflation increased by 5.91%, the highest it has been in the past seven years. As a result, domestic demand for consumer goods posted a weaker performance than the same period last year, with an increase of 9.8% compared to 14.4% in 2019. This is the lowest growth rate since 2014, according to The General Statistics Office of Vietnam.

Within the fast-moving consumer goods (FMCG) industry, the spread of COVID-19 is disrupting businesses, but not all categories and retailers will see a negative impact. Kantar is closely monitoring the impact across different shopping channels to shed light on how consumers’ behaviours are changing, to help brands and retailers to respond to them in this VUCA (volatile, uncertain, complex, ambiguous) time.

1. More stocking up and less socializing

Based on Kantar Worldpanel data, Vietnam’s FMCG market growth shows a slowdown in the first two months of 2020 despite 2019’s optimistic picture. The dairy, packaged foods and personal care caetgories have managed to sustain growth while beverages has suffered a decline despite this being high season (Lunar New Year aka Tet). This is possibly explained by the lower numbers of parties and celebrations as Vietnamese people avoided socialising and gathering in a bid to reduce their exposure to the virus.

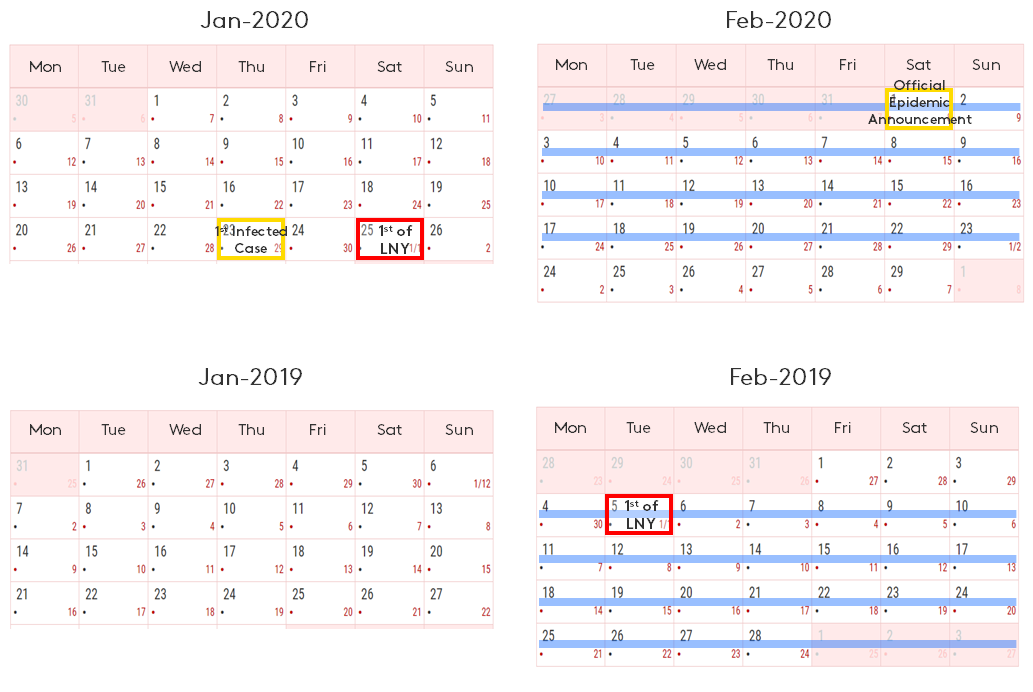

In order to deep dive into the impact of COVID-19, which started from the week right after Tet Eve (the first day of Lunar New Year), we have realigned the reporting period based on the lunar calendar to make the data really comparable. By looking at consumer purchase behaviour in the four weeks after Tet 2020 (post Tet period) compared to the same period last year – four weeks after Tet 2019, we are now able to see how COVID-19 has initially affected Vietnamese consumers’ FMCG spend and purchase behaviour

*Blue line: Data period 4 weeks ending 23 Feb 2020 vs 4 weeks ending 3 Mar 2019

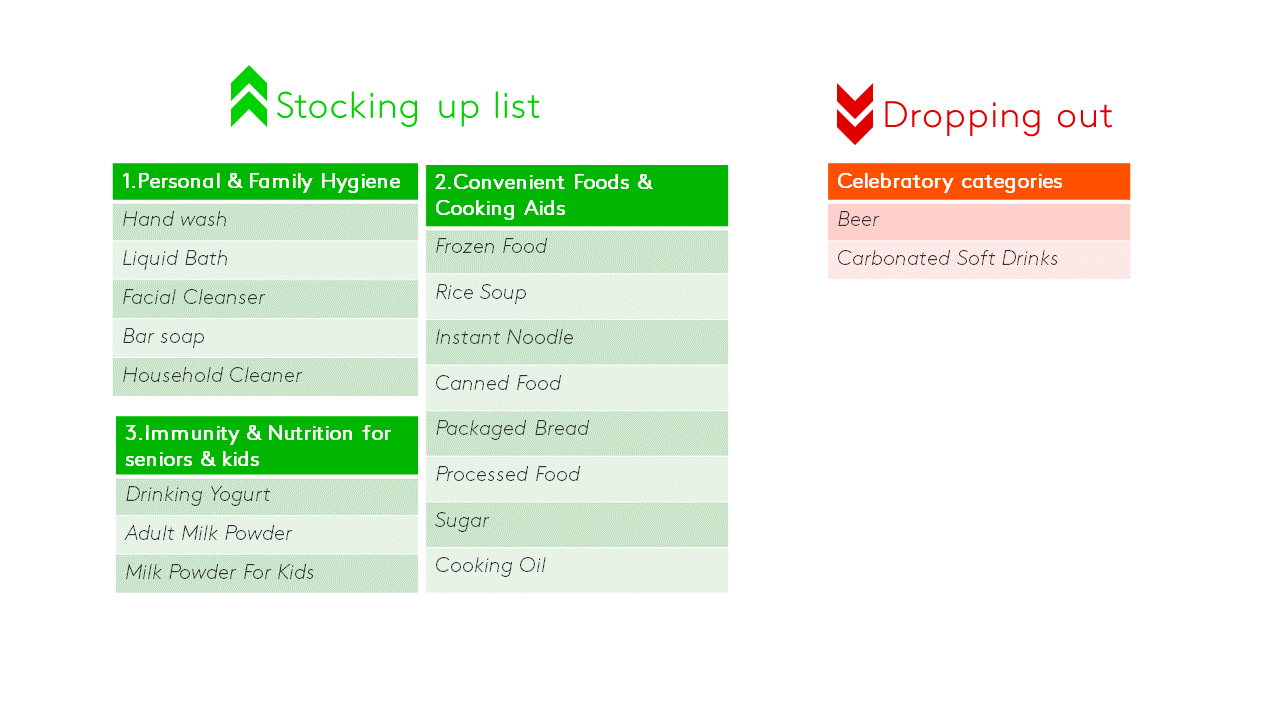

Vietnamese consumers in the four key urban cities show a tendency to stock up across three groups of categories. Firstly, they spend more on categories that offer personal and family hygiene in order to remain clean and kill germs. Hand wash, bar soap and household cleaning products are all seeing double- and even triple-digit rise. Secondly, convenience foods and cooking aids also surge during the outbreak, as people eat at home more probably due to the fear of catching the virus as well as the extended home stay of children who haven’t been at school. Frozen food, canned food, instant noodles and cooking oils are a few categories enjoying impressive growth. The other group of categories that consumers seek for during this time are immune-boosting and nutrition products, especially for seniors and kids who are at higher risk. Therefore, speciality milk powder and drinking yoghurt are more favoured to stay healthy.

On the end of the spectrum, consumers are cutting celebratory categories from their basket during the spread of coronavirus. Beverages including both alcoholic drinks and non-alcoholic categories have suffered the most in this period. Beer and carbonated soft drinks are, in particular, experiencing a sharp decline.

2. Channel movements

There are changes not only in consumers’ baskets but also in their channel choice during the virus outbreak. Online shopping prevails and booms significantly thanks to the increasing number of transactions, accelerating the growth of online FMCG spend to a triple digits just in the month since the official announcement in Vietnam. This trend is expected to continue in the coming months, especially when there has been advice from local authorities to shop online in order to avoid crowds and physical contact.

With the surge in demand for protection masks and hand sanitisers among the Vietnamese, it’s no surprise to see the robust growth of consumer spend in pharmacies and drugstores including Medicare and Guardian. More purchases of hygiene products were made in these channels as consumers’ priorities for now are to protect and enhance their safety.

As the number of affected people swells, this results in panic buying among the Vietnamese in some areas, especially where there have been confirmed cases. It drives demand for stock-up, leading to the notable growth of major modern retail formats including hypermarkets, supermarkets and minimarkets. Part of the attraction of these formats is that they offer hygiene, product variety, and lots of epidemic supporting programs such as home-delivery, stable-price masks and hand sanitiser, farmer supporting sales etc. Within the big retail format, Big C is one of the key retailers to achieve a strong performance, driven by increasing both footfall and spend per trip in its stores. MM Mega market (the cash-and-carry retail model) has also picked-up during this time despite its downturn in recent years.

Meanwhile, shopping in those places most commonly used for daily needs are losing traffic as shoppers preferring “less physical contact” and make fewer shopping trips but with a bigger trip size. As such, street shops – key shopping channels, and convenience stores are seeing a short-term impact caused by the COVID-19.

Food for thought

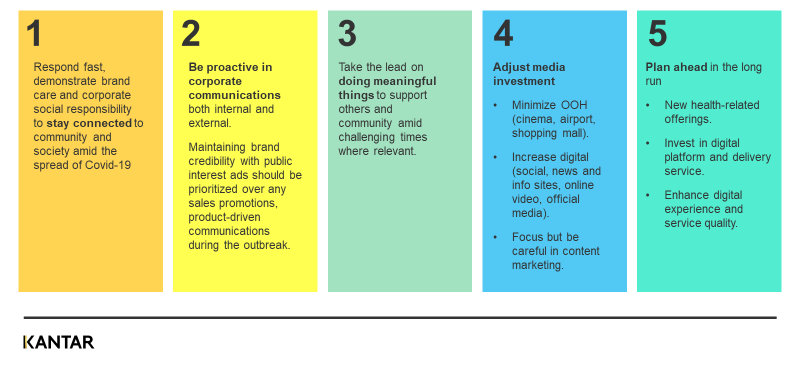

The unexpected virus outbreak remains on-going with more and more people affected. Economic activities and business operations have been continuously disrupted. Below is some food for thought to stay safe and strong during challenging times and to be well-prepared in the post-pandemic period.

The VUCA (volatile, uncertain, complex, ambiguous) situation has been escalating very quickly in the last two months, posing challenges for all of us. In order to understand how this context may impact purchase behaviours and how brands may be able to mitigate associated risks, we are continuing to closely monitor the impact of COVID-19 pandemic across FMCG categories and retailers, on a monthly basic. Contact us to discuss on what we can support you to deal with the crisis.

Notes to editors:

*The analysis is based on Worldpanel data, household panel in Urban Vietnam 4 key cities (Ho Chi Minh City, Ha Noi, Da Nang and Can Tho), total FMCG excluding Gift for in-home consumption.

Data period: 4 weeks ending 23 February 2020 versus 4 weeks ending 3 March 2019.