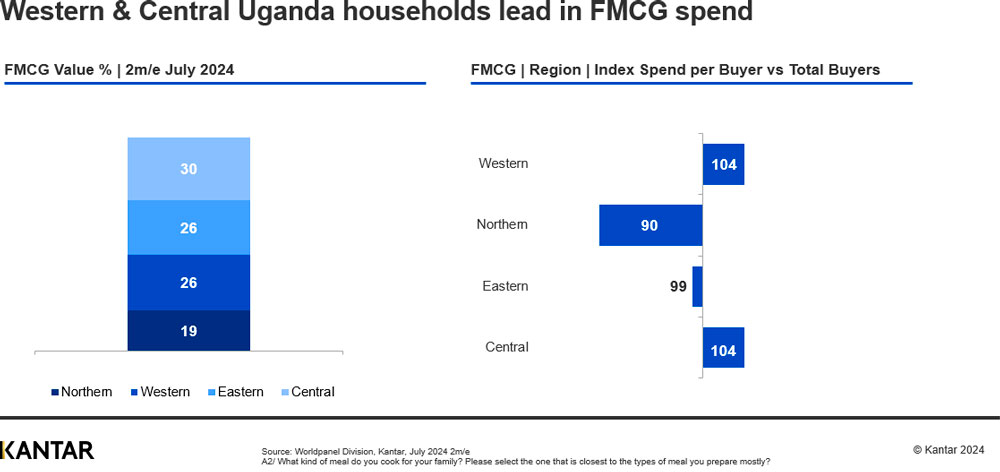

A Nation of Contrasts in FMCG Spending

Ugandan households are not uniform in the way they purchase FMCG products. There are clear differences in purchasing intensity between regions, with Central and Western Uganda showing higher levels of spending. These regions benefit from better access to retail outlets, higher urbanisation and greater income stability. In contrast, Northern Uganda is significantly below the FMCG spending index due to lower income levels and limited distribution infrastructure.

In areas where incomes are lower or spending power is more limited, one solution gaining traction is the use of Low Unit Packs (LUPs), smaller, more affordable product formats that allow shoppers to buy essential items in quantities that suit their budgets. These packs are especially particularly in price-sensitive and rural areas where consumers prioritise affordability over quantity.

Food leads FMCG spend

Food is the top spending category for Ugandan households, accounting for around 27% of their FMCG spending, more than any other category. Although food is already a major focus for most people, there's still room for growth. Wealthier households spend a lower proportion of their FMCG budget on food than lower income groups. For example, households in Eastern and Western Uganda spend just 25% and 17.9% respectively on food, both below the national average of 27.3%. A similar trend is seen among Gen Z and Millennials, who also spend slightly less on food than older age groups. These patterns show that food is important to everyone, but with the right strategies for different groups and regions, brands can grow even more.

Engage gen Z and millennials: unlocking future spend

There is significant potential to improve communications with shoppers who are currently under-indexed in their FMCG spend, particularly Gen Z and Millennials. While these younger age groups have greater spending potential, their engagement remains limited. For example, shoppers aged 18-24 account for over 20% of FMCG value, but under-index in their spend at just 94 compared to the average. To unlock this future value, manufacturers must focus on targeted communication and engagement strategies. These efforts are essential to effectively drive FMCG consumption among Gen Z and Millennial households, where significant growth opportunities lie.

Growing FMCG through kadukas and affordable packs

Kadukas, small informal shops found in Uganda's neighbourhoods, are the heartbeat of the country's FMCG trade. Despite the rise of supermarkets in urban centres, kadukas remain dominant accounting for a remarkable 82.1% of total household FMCG spending. These stores are perfectly positioned to distribute LUPs.

Uganda’s FMCG landscape is far from uniform with regional, social class and generational differences, alongside their evolving retail formats, creating both challenges and opportunities. By tailoring their strategies to the unique needs of different consumers, brands can achieve meaningful growth in the evolving market.

To explore the full findings of this report or access more specific category reports, contact us today.