Despite an expected slowdown in overall GDP growth to 1.6%, due to a drop in oil sector outputs, Saudi Arabia's non-oil sector – including FMCG – is projected to expand 4.6% this year. This positive outlook presents opportunities for brands and retailers.

Economic conditions in Saudi are improving. Domestic demand remains robust, while inflation is easing slightly – dropping from 3.4% in January 2023 to 2.7% in February and March. However, it’s likely that consumers may continue to become more price-sensitive, seeking out discounts, promotions, and lower-priced alternatives. They may also prioritise essential goods over discretionary items, and adjust their consumption patterns.

The volume-value gap

In the Saudi market, pricing pressures are widening the volume-value gap. While inflation has plateaued, steep price rises persist and are impacting all FMCG segments.

This is especially the case in essential categories like dairy – where price increases jumped from 9.5% in June 2022 to 17% in March 2023, and food, with a jump from 7.9% to 12.5%.

This ongoing trend requires brands and retailers to analyse price-volume-value dynamics, adapt their pricing strategies to changing consumer behaviours, and focus on value and innovation.

Target Saudi and young buyers

Saudi buyers have greater purchasing power and contribute more value to the FMCG market than expats in the region. This makes it crucial for marketers to engage with this audience to drive success.

Capturing the loyalty of younger consumers is also key. While they contribute a lower share of volume and spend, they are willing to pay more for FMCG products – and marketers should leverage this opportunity.

Understanding the interplay between spending power and price consciousness across different socio-economic groups opens strategic opportunities for tailored offerings.

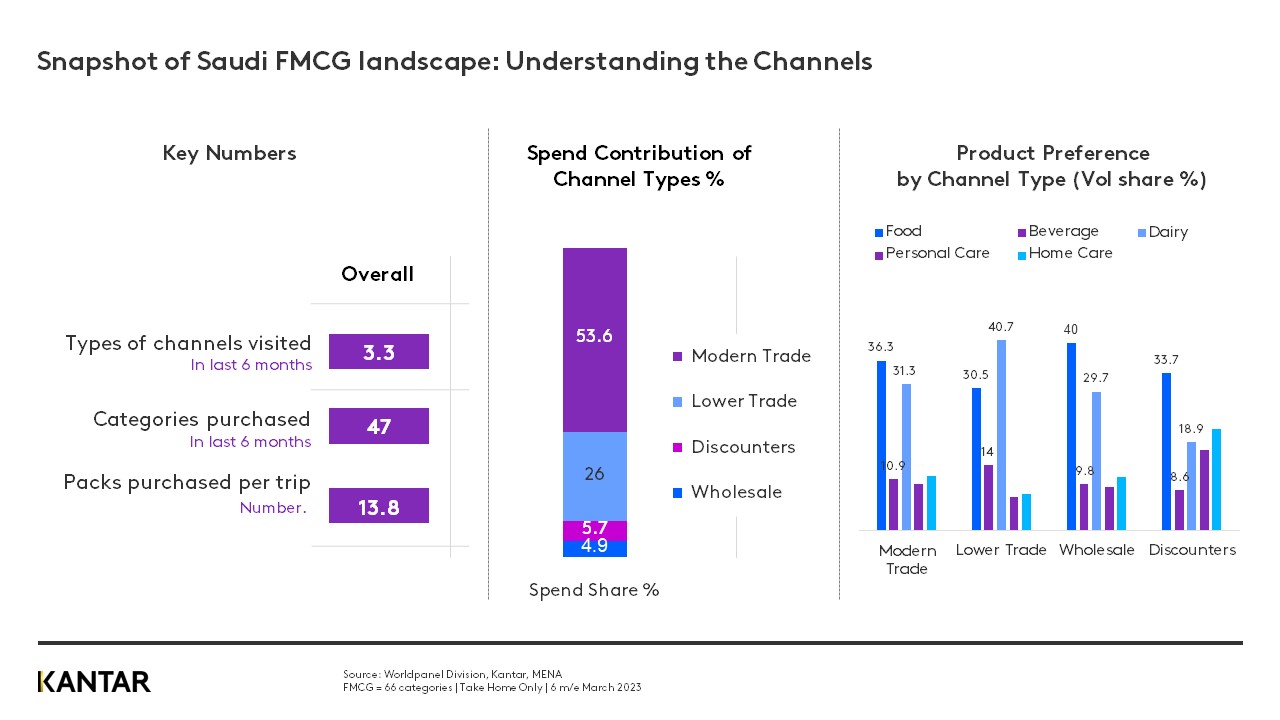

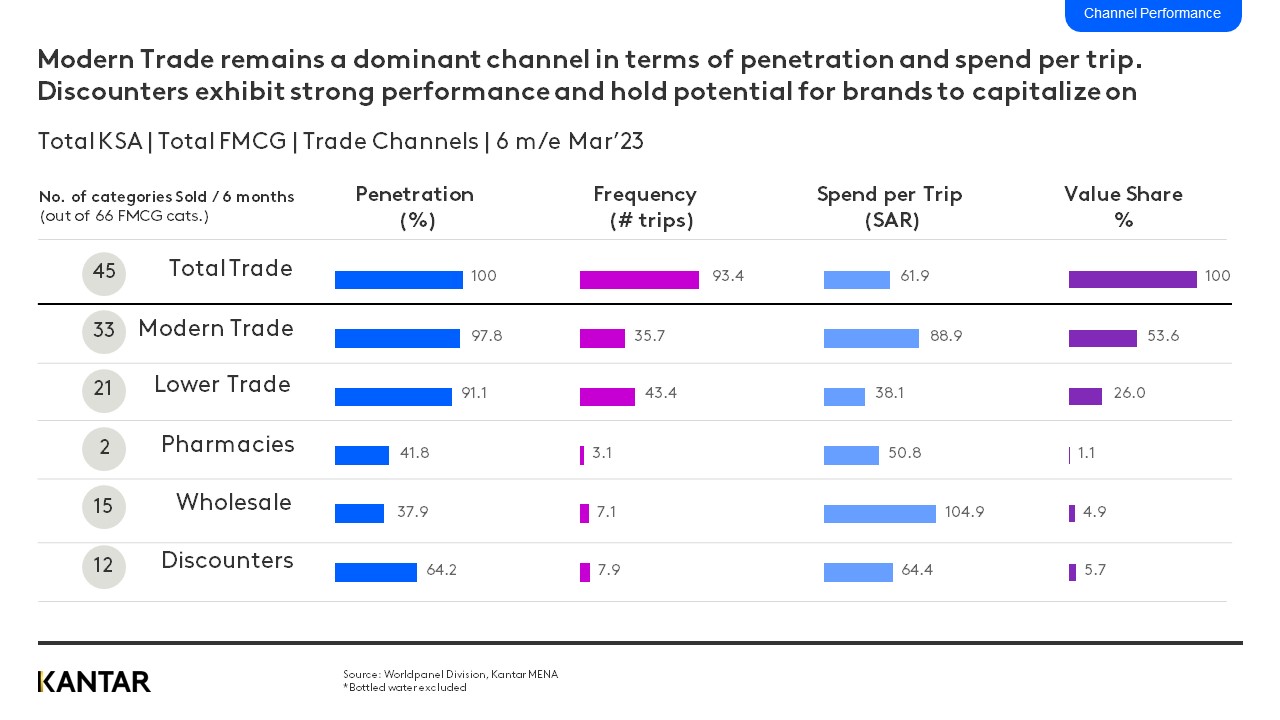

Discounters hold significant potential

Modern trade remains the dominant FMCG channel in Saudi Arabia, in terms of penetration, spend per trip and value share. Discounters are performing strongly, and brands should capitalise on their soaring popularity: they now reach 64% of the region’s population. More than a dozen discounters have emerged in recent times – including Economic Hall, Jeddah, and Dammam – offering shoppers a broader range of options and potentially lower prices.

Leveraging the high penetration and developing depth of the discounter channel presents an opportunity for significant sales growth, especially for brands in the personal care and home care categories.

Discounters appeal to a diverse shopper base, across a range of nationalities and socioeconomic groups, and are favoured by younger consumers.

To unlock the full potential of the thriving Saudi FMCG market, brands must foster stronger relationships with young shoppers, strengthen partnerships with discounters, and optimise pricing strategies. Continuous monitoring of market trends and consumer preferences will ensure sustained growth and competitiveness.

Fill in the form below for more insights.