It has never been harder for FMCG brands to grow their footprint in Latin America. While the region’s GDP grew by a very healthy 2.3% in 2024, food price inflation was double the market average at 14%.

In response, shoppers made fewer trips to stores – and lower purchase frequency means reduced opportunities for brands to be bought. Consumers also reprioritised what they put in their baskets, switching from one brand to another to ensure they could keep enjoying their favourite categories while balancing their budgets. This has eroded loyalty, as the average number of brands purchased per shopper increased.

The result: 61% of the brands in Worldpanel’s 2025 Latam Brand Footprint ranking were chosen fewer times than in 2023, leading to a drop in Consumer Reach Points (CRPs).

Super brands – those with penetration above 70% – were most affected, with just over a third (34%) increasing their CRPs. However, the super brands at the top of the ranking continue to stand tall, with a remarkable number of CRPs to their name. Coca-Cola remains the most chosen brand in Latin America, with 2.9 billion CRPs, followed by Colgate (804m), Pepsi (598m), Lala (534), and Bimbo (534m).

Medium-size brands performed best across the region, with 41% growing their footprint. Only Latam’s smaller brands were able to achieve a modest increase in purchase frequency.

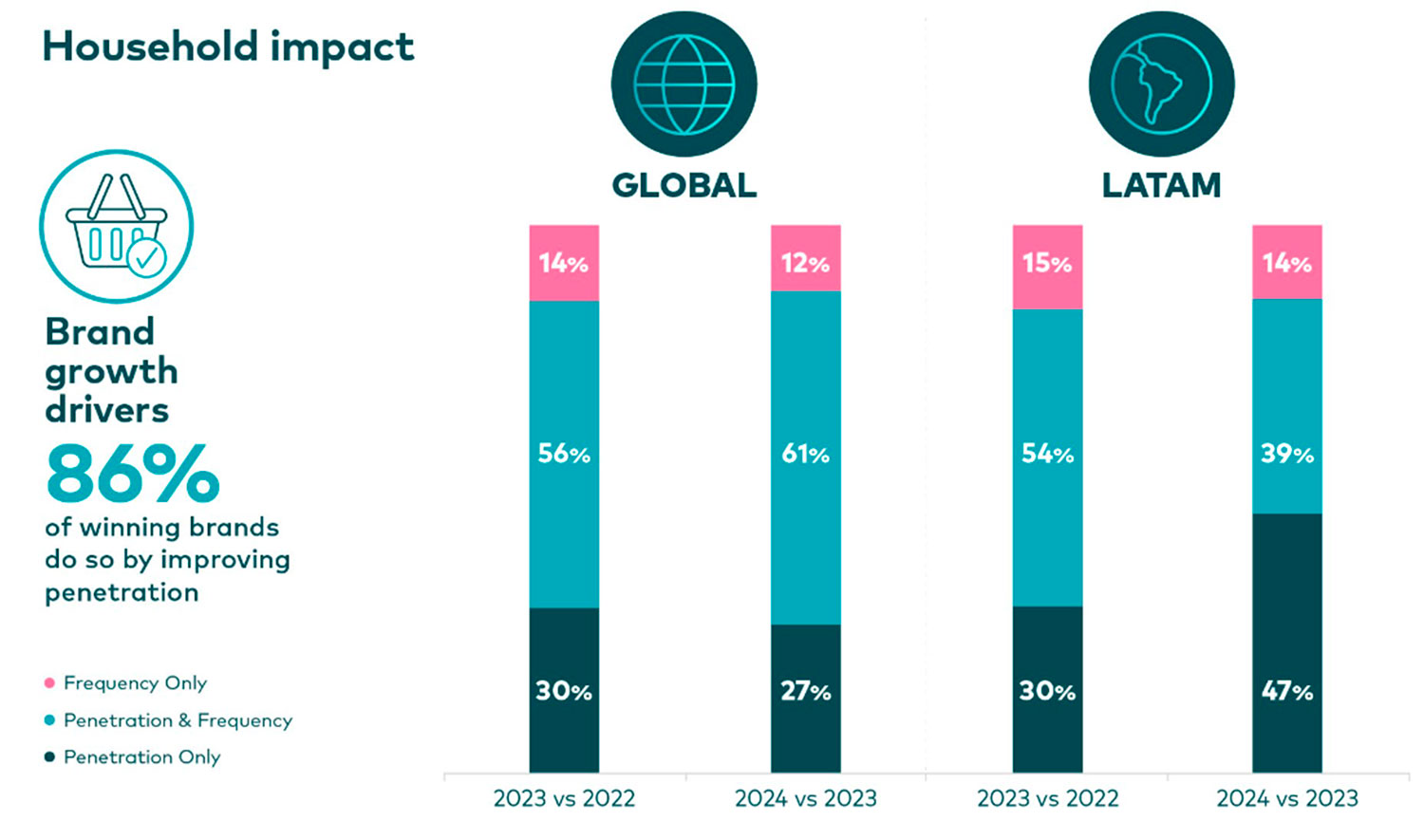

The penetration principle

The majority of those brands that did manage to overcome the obstacles to growing their footprint had one key factor in common: they successfully expanded their buyer base.

Boosting penetration is the most effective growth driver in the Latam region, with 86% of the brands that gained CRPs in 2024 doing so by attracting new shoppers, and 47% growing exclusively through this strategy. The principle remains consistent regardless of a brand’s size.

Expanding reach can be accomplished through a number of approaches, including diversifying the product portfolio, targeting new occasions, or conquering white spaces.

Fragmented purchase behaviour

In 2024, each Latin American consumer shopped across 8.9 different channels on average throughout the year. Channels play a really decisive role in the shopping journey. Especially in high-frequency categories such as snacks and beverages, Latinos are more likely to switch brands than channels.

The challenging growth environment within Latin America makes it crucial for brands and retailers to build an in-depth understanding about the shoppers who do not buy their products or visit their stores – and why – while driving repeat purchases and trips among those who do.

This is rendered even more important given that the future economic outlook for the region remains uncertain. GDP forecasts have been cut, with expectations curtailed by US tariffs, global trade volatility, and weaker external demand.

The 2025 Brand Footprint report provides a detailed view of the dynamics shaping consumer choice in Latin America. The insights in its pages are based on Worldpanel’s tracking of real purchasing decisions across 15 markets, 5,800 FMCG brands, and more than 50,000 panellists representing 90% of households in the region.

Read the report to discover how the winning Latam brands have surmounted the barriers to growing their buyer base and achieving penetration-led growth.