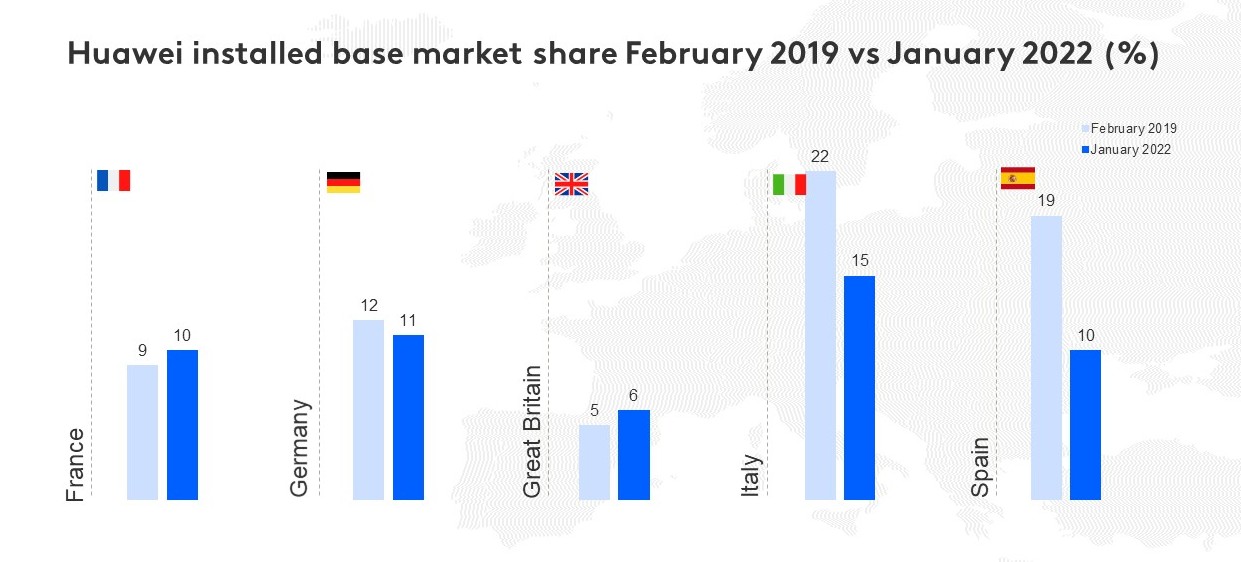

A lot can happen in three years, especially in the smartphone market. In February 2019, Huawei was on what seemed to be an unstoppable growth trajectory in Europe, cracking tough premium markets such as Great Britain and Germany and solidifying its share in Southern Europe. Kantar’s Worldpanel ComTech tracking service found that they gained 9 million net new customers in the 12 months to February 2019 across the “EU5” markets (France, Germany, Great Britain, Italy and Spain).

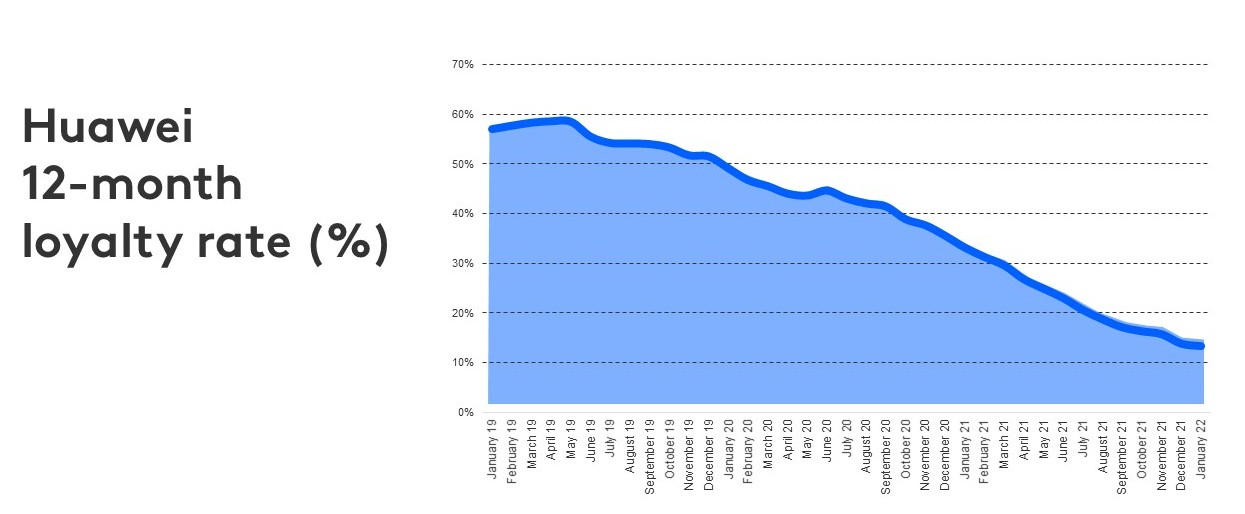

Yet a Trump Presidency and Chinese trade war resulted in them being added to the US Entity List in May 2019. Google subsequently withdrew Android support from Huawei devices, and the omission of popular apps made them an untenable choice in many consumers’ eyes.

Fast forward three years and things look very different. In the 12 months to January 2022, Huawei lost 7.4 million customers.

Acquisition opportunity fuelling C-brand growth

However, Huawei still has a sizeable base of smartphone owners: there are 25 million of them across the EU5 alone. Many of these consumers are now close to or at the point of upgrade: the average length of smartphone ownership in Europe is at 2.5 years, and over half of Huawei’s base have owned their device for this length of time or more. A mammoth acquisition opportunity naturally presents itself for competitors, with Huawei retaining a diminutive 13% of those who purchase a new smartphone.

As one door closes, another opens. Chinese brands Xiaomi and Oppo are experiencing strong growth in Europe, fuelled in the most part by Huawei churners. Across the EU5, 23% of Xiaomi’s acquisition, and 28% of Oppo’s, is made up of former Huawei customers. This opportunity is set to increase as more Huawei customers leave the brand in the coming year.

Xiaomi has 13% installed base share across the EU5, with strong performance in Spain and Italy, where it has secured the #1 and #2 smartphone spots with 33% and 19% share respectively.

What’s aiding Xiaomi’s success?

Competitive pricing is a key driver behind Xiaomi’s success. Lei Jun, Xiaomi’s founder, set the cap on the product net profit margin to a maximum of 5%, including smartphones. This has resulted in Xiaomi being incredibly competitive in the lower value market: 90% of Xiaomi devices owned cost €400 or under. But this highlights a weakness Xiaomi are struggling to overcome – landing a credible, premium flagship handset. This is needed to gain significant share in premium markets such as Great Britain and Germany – Huawei’s first successful premium phone was the P20 that launched at €650, securing them a strong foothold in the British market.

Another driver behind Xiaomi’s success is its focus on R&D and innovation, constantly challenging what’s possible. Internally, Xiaomi refers to it as the ‘ABCDs’’, referring to Audio, Battery, Camera and Display. This appears to be working – consumers that own Xiaomi phones were much more likely to seek out: battery life (55%), camera quality (51%), screen size (44%) and storage capacity (40%). Doing a common thing uncommonly well can lead to great success.

Challenges remain

However, with Xiaomi’s base beginning to mature in Spain (over 1 in 3 have now owned their device for over 24 months) it faces a new challenge: retention. In the 12 months to January 2022, 68% of Xiaomi’s base that purchased a new phone remained loyal; this loyalty rate has dropped versus the previous year. As more of Xiaomi’s base mature, this will likely fall further. These churners are mostly moving to Samsung, but interestingly also migrate to Apple and Oppo. They are also willing to spend a greater amount on their next phone, with 1 in 4 spending €800+.

Oppo: one to watch

Huawei’s churn is set to intensify throughout 2022, presenting a sizable acquisition opportunity for both existing and new players. Oppo is a brand to watch, growing its share throughout the European markets and gaining 2.5 million net new customers in the 12 months to January 2022. Having announced its latest flagship model, the FIND x5, on 24 February, Oppo begins the year on a strong platform for success. Its strategy is altogether more premium, with 8% of current Oppo owners spending €800 +. 1 in 10 of its new customers have moved from a previous Xiaomi device, (whereas less than 1% of Xiaomi acquisition has come from Oppo), suggesting its growth could accelerate as Xiaomi churn increases.

A lot can happen in the smartphone market in the next three years. Reach out to our experts for more insights.