With value sales growth of 5.6%, there was a marked improvement in Mainland China's FMCG market during the fourth quarter of 2023 compared to the same period the previous year, which was heavily affected by the pandemic. Looking at the year as a whole, a moderate recovery is in evidence, with growth of 1.2%.

In terms of categories, beverages and household cleaning products maintained significant growth in Q4. Food, dairy products, and personal care showed signs of recovery, although at a slower pace than the market average.

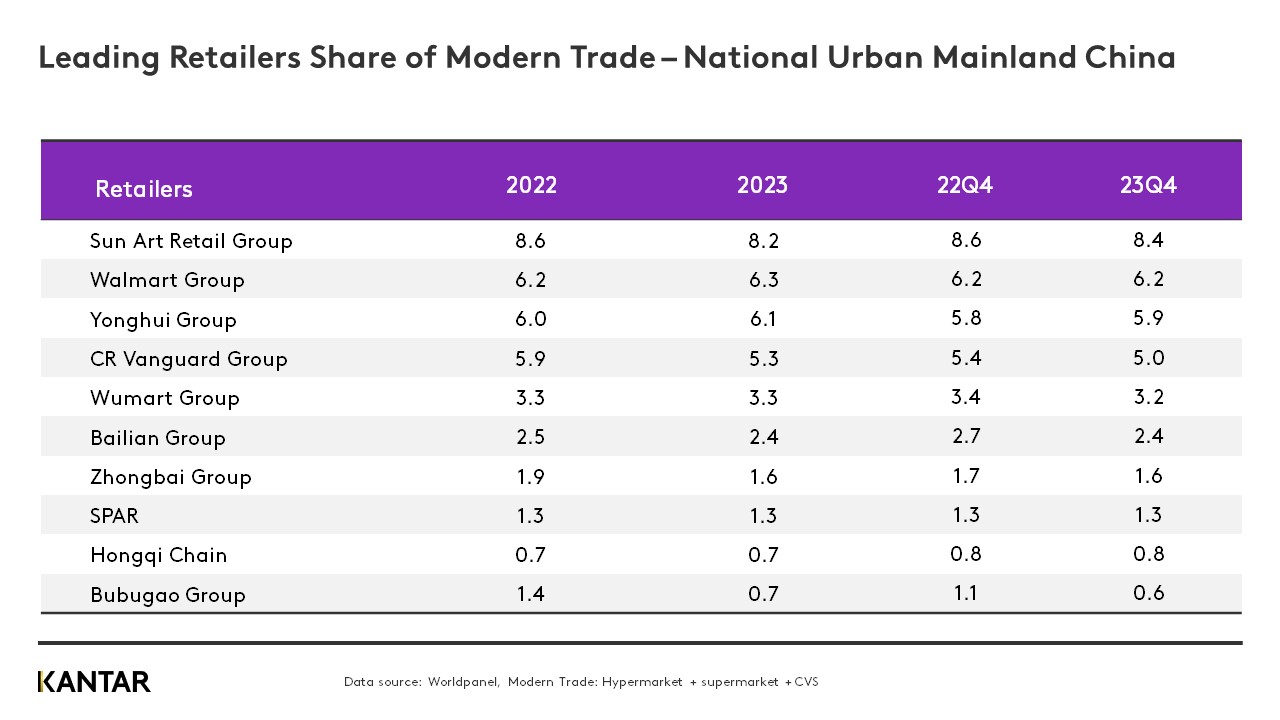

The performance of modern channels, in particular hypermarkets and large supermarkets, resurged compared to the previous year's downturn. Throughout 2023, Walmart and Yonghui both increased their share amongst fierce competition. However, the total FMCG market share held by the Top 10 modern trade retailers decreased by 1.6% – an indication of fragmentation, and increasingly diversified formats.

Membership stores continued to grow in Mainland China in Q4, but more slowly than the first two quarters of 2023, due to saturation in upper-tier cities and intensified competition. This may lead to an emerging trend of membership stores expanding into lower-tier cities.

Here are five outlooks for Mainland China’s retail market in 2024:

1. Small formats are becoming big business

In 2023, consumers maintained their habit of shopping in proximity channels. Although a decrease in average spend per trip led to a slight slowdown in the growth of small-format sales, small supermarkets and convenience stores continued to successfully enhance the shopping experience, for instance through developing new service offerings.

This year, proximity channels will encounter a general slowdown in the growth of consumer spending, and increased competition. Small-format brands must enhance their supply chain operations and digital capabilities. Large-format brands are opening smaller community stores, streamlining SKUs, and increasing investment in fresh produce.

2. Traditional retailers and membership stores will vie for dominance

In 2023, the decline of sales in hypermarkets accelerated, and their performance was surpassed by large supermarkets, which are also on a downward trajectory. Large-format retailers will continue to confront significant challenges. Only through transformations – such as product differentiation, supply chain optimisation, establishment of distinctive stores, and refined operations – can they survive the intense competition.

Over 10% of Mainland Chinese households purchased FMCG from membership stores in 2023, with sales increasing 40% compared to 2022. In the short term, foreign retail giants such as Sam’s Club and Metro will maintain their advantage. Domestic brands are introducing products better suited to the daily needs of consumers, with smaller package sizes and more aggressive pricing strategies.

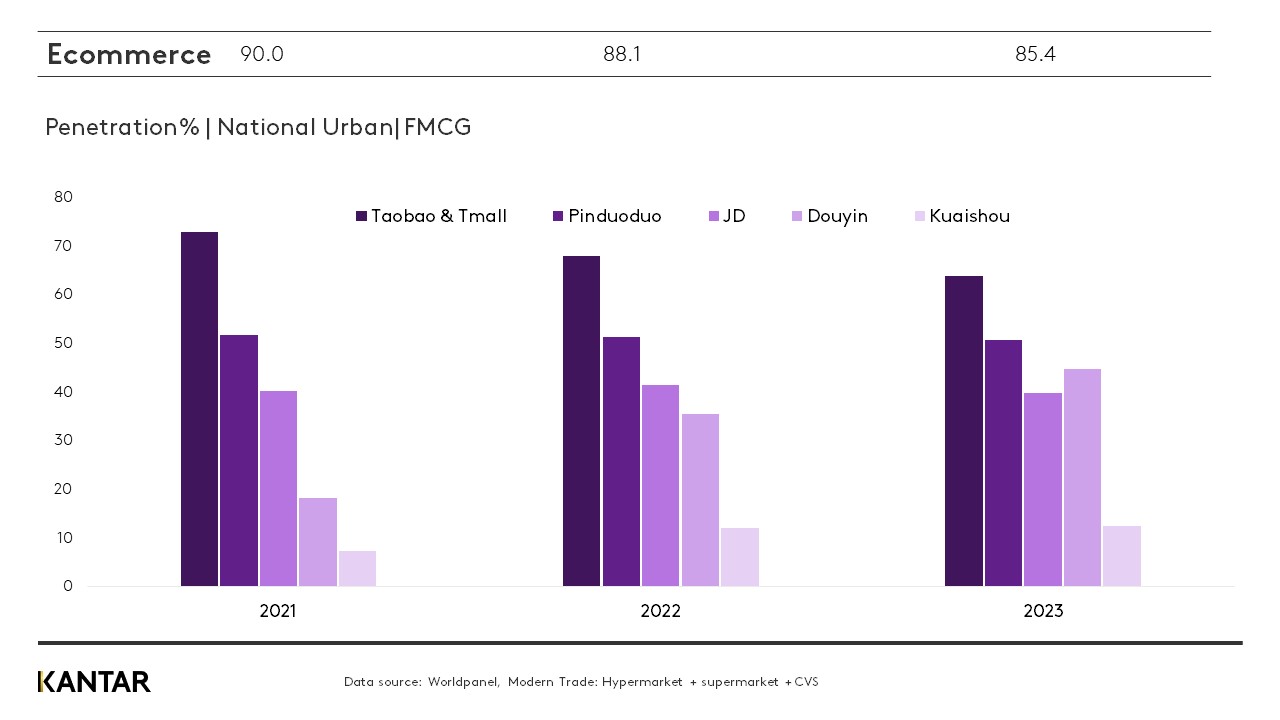

3. E-commerce will shift from 'low price' competition

In 2023, as life returned to normal, some consumers reverted to in-person shopping, leading to a nearly 3% decrease in the penetration of e-commerce. However, there was a significant increase in purchase frequency, leading to overall sales growth of 5.3% for the year.

As consumers shop around, decreasing their loyalty, low-price marketing alone cannot stimulate additional growth. To establish long-term price advantages in consumers' minds, platforms must improve supply chain efficiency, and reduce fulfillment costs.

The strong rise of interest-based e-commerce has significantly disrupted traditional shelf-based e-commerce. More than 40% of Mainland Chinese urban households purchased FMCG from the Douyin platform in 2023, and its penetration is expected to surpass Pinduoduo this year.

4. Community group buy (CGB) landscape is consolidating

Following three years of rapid growth amid the pandemic, O2O growth slowed in 2023. Meanwhile the established CBG giants gradually withdrew and consolidated their operations. With penetration nearing 25%, Meituan Youxuan and Duoduo MaiCai are expected to continue to dominate.

5. The expansion of discount formats accelerates

In 2023, the discount store format surged across all categories. Established less than four years ago, Hotmaxx now has more than 600 stores, while Hema Outlet opened its inaugural store in 2022 and presently operates over 70 stores. Discounters are improving operational efficiency by engaging in large-scale production, and selling their own-brand products.

Specialist snack discount stores became popular nationwide in 2023, with more than 7.6% of Chinese urban households purchasing from these in Q4.

As traditional retailers increasingly join the discount game, competition will not only centre on superficial price rivalry. Building and operating 'vertical supply chains' will be vital.

If you would like to learn more, please get in touch with our experts or access our data visualisation tool to explore current and historical grocery market data for Mainland China.