A study from Kantar’s Worldpanel division in the United States revealed key trends in the Video-on-Demand (VoD) market between January and March 2025. New service acquisitions fell by 11% quarter-over-quarter (Q1 2025 vs. Q4 2024) — a smaller decline compared to the 17% drop seen in the same time period a year ago (Q1 2024 vs. Q4 2023). Paramount+ attracted the highest share of new video streamers, at 11% market share, capturing nearly 50% of its new subscribers through the Yellowstone franchise (including 1923 and 1883) and its popular Western and historical dramas. Netflix ranked second, drawing more than a third of its new subscribers, largely thanks to WWE sports programming. Tubi also gained traction, attracting 1 in 20 of its new users through NFL and motorsports content, underscoring the growing role of sports in ad-supported streaming tiers. Meanwhile, Apple TV+ led among SVOD services in new subscriber acquisition, securing 1 in 4 new SVOD subscribers, with 44% of them citing hit series like Severance and Silo as their main reason for signing up.

In the first quarter of 2025, the video streaming sector continued to stabilize, with the number of households accessing streaming services staying steady quarter-over-quarter, showing no more than a 2-percentage-point quarterly increase since Q4 2023. This plateau highlights the growing challenge for platforms to expand their reach in a saturated market, where the average number of services per household remains steady at six, with no significant change year-over-year or quarter-over-quarter.

The seasonal dip following the holidays resulted in an 11% decrease in new subscriptions between Q4 2024 to Q1 2025, a notable but less steep decline compared to the previous year’s 17% drop, between Q4 2023 to Q1 2024. With platforms now facing a more mature audience base, while churn is still high, the absence of sharper declines in cancellations suggests that viewers may be finding more value in their current subscriptions or have become more discerning about which services they are willing to keep. This reflects a broader industry trend of maturation, as streaming services are increasingly navigating the transition from explosive growth to a phase of customer retention and content differentiation. This mirrors a broader shift within the video streaming market, where platforms are adapting to a more competitive, saturated landscape. Instead of aggressive expansion, companies are focusing on maintaining a loyal customer base while diversifying content and improving user experience to fend off the potential for deeper churn.

Franchise and Premium Content Drive Subscriber Gains as Streaming Services Navigate Saturation

In Q1 25, Paramount+ wins among overall new service uptake, capturing nearly half of its new subscribers through specific content titles. Central to this surge is the creation of a dominant "Yellowstone" franchise universe, which spans multiple series including 1923, and 1883, this allows Paramount+ to retain and grow its fan base.

In addition to its franchise strategy, Paramount+ has also leaned into the popular Western and historical drama genres with “Landman”, bolstering the appeal of its content portfolio and cementing its place in the hearts of viewers. This approach demonstrates the ongoing significance of franchise-driven content in acquiring and retaining subscribers, offering a tailored experience that meets the demand for high-quality, immersive storytelling.

Netflix, while second in terms of new subscriber acquisition, continues to attract a significant portion of the market (10%). The platform's success is driven primarily by specific content, with sports programming — particularly WWE — being the standout title driving acquisition. This emphasizes the growing importance of live sports in streaming platforms’ content libraries, providing a lucrative draw for new users who seek premium, real-time one-off entertainment events.

Similarly, Tubi, the free ad-supported service, also taps into the sports-loving audience, with nearly 1 in 20 of its new users joining the platform to watch NFL and motorsports content, like NASCAR. In both paid and free ad-supported tiers, competition is heating up, as the top five services vying for new users are closely packed — with less than a 2-percentage point difference between the number one and fifth place providers. This crowding illustrates the growing popularity and increasing competition in the ad-supported streaming space, which now reaches approximately 85% of the U.S. population.

In the SVOD space, Apple TV+ stands out as the top acquirer of new subscribers, capturing a remarkable 1 in 4 new subscribers in Q1 2025. Like Paramount+, Apple TV+ benefits from the appeal of specific content, with 44% of its new subscribers citing particular series as the reason for signing up. Among these, the critically acclaimed sci-fi series Severance and Silo, which have earned Golden Globe, Critics Choice, Emmy, and BAFTA nominations, have proven particularly effective in drawing audiences to the platform. This illustrates the growing importance of high-profile, award-nominated content in attracting subscribers to premium services, which are positioning themselves as home to top-tier programming.

Evolving through interface and infrastructure to meet the expectations of a maturing audience base

As the video streaming industry continues to mature in 2025, user experience has emerged as a pivotal factor influencing subscriber satisfaction and retention. While overall content satisfaction has remained stable year-over-year, a notable increase in dissatisfaction has led to a decline in net satisfaction scores. This shift suggests that, beneath the surface, users' expectations regarding interface and infrastructure are evolving, highlighting areas where streaming platforms must innovate to maintain competitive advantage.

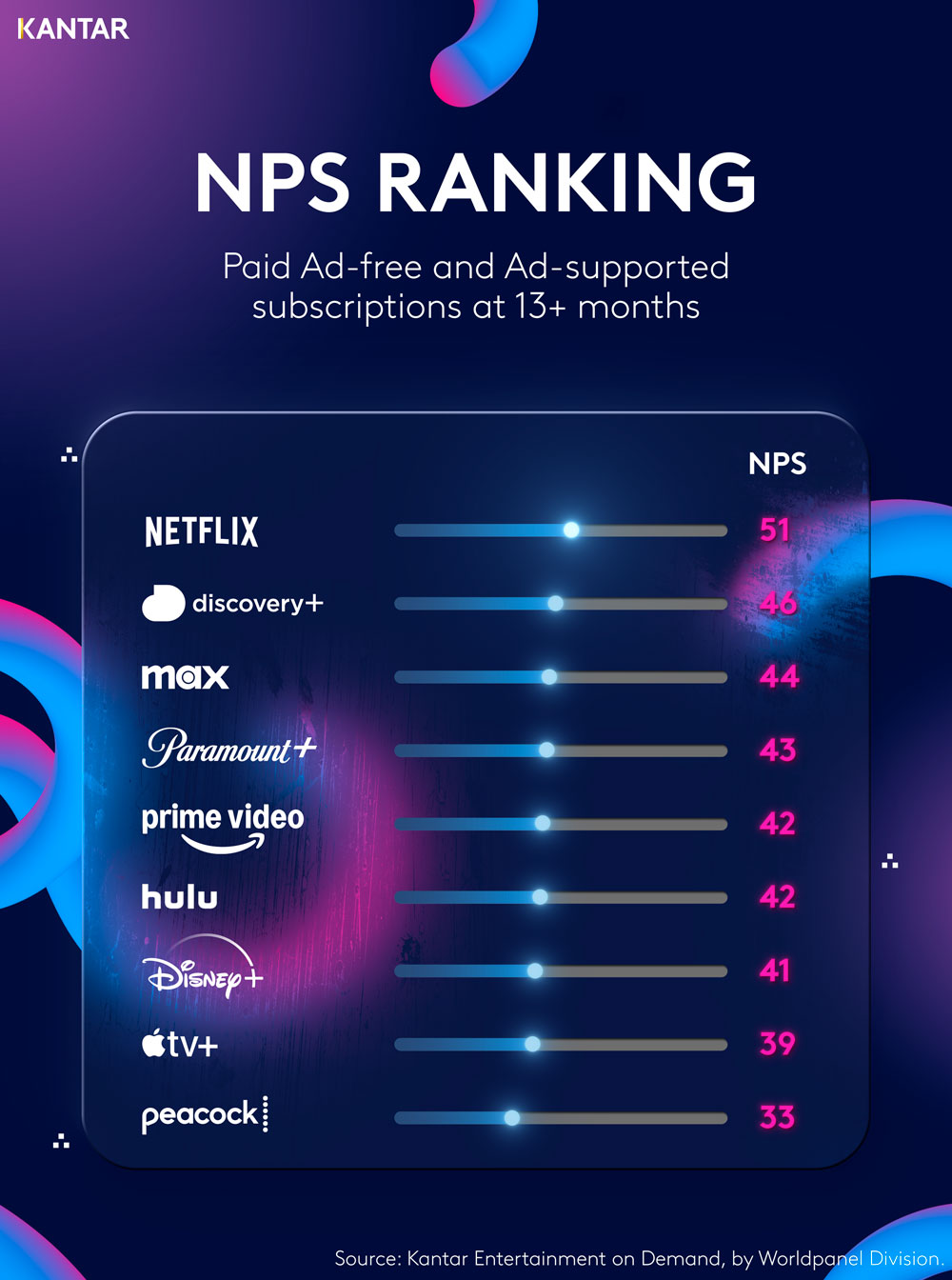

Despite improvements in certain aspects, such as TV interface navigation and fast-forwarding functionalities, fundamental elements that facilitate content discovery have seen a rise in dissatisfaction. Key drivers like search functionality and overall interface usability have not met user expectations, indicating that enhancements in these areas are crucial for improving the user experience. Interestingly, longer subscription tenure correlates with higher satisfaction levels and NPS, particularly when users find the interface intuitive and search capabilities efficient. This trend underscores the importance of a seamless and user-friendly experience in fostering long-term customer loyalty.

Leading platforms are responding to these challenges by investing in significant user experience improvements. Netflix, for instance, has implemented a redesigned TV homepage after over a decade, aiming to enhance content discovery and user navigation. Additionally, the introduction of interactive search features leveraging generative technologies seeks to make content discovery more dynamic and responsive to user queries. Similarly, Max has focused on advanced search capabilities, including voice search and AI-driven content recommendations, to provide a more personalized and efficient user experience. These initiatives reflect a broader industry trend where platforms are prioritizing user experience to differentiate themselves in a competitive market.

Access the interactive data visualisation for more information.